AUTHOR

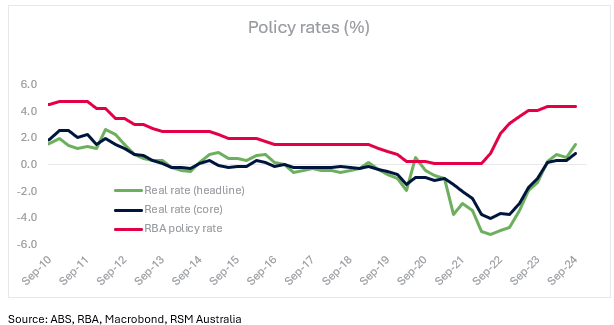

Australia's recovery in 2025 will be cautious as the RBA ends its policy easing cycle at 3.35% by December 2025.

The labour market remains resilient, but stricter immigration policies and ageing demographics pose long-term challenges to growth.

Global trade risks, rising insolvencies, and stricter lending standards could further strain the economy's recovery path.

Australia is set for a cautious recovery and stabilisation in 2025, underpinned by moderating inflation, strategic policy adjustments, and evolving consumer behaviour.

The Reserve Bank of Australia (RBA) is expected to hit the brakes on policy at 3.35% by end-2025, cementing a shift to a higher-cost borrowing environment for businesses and households.

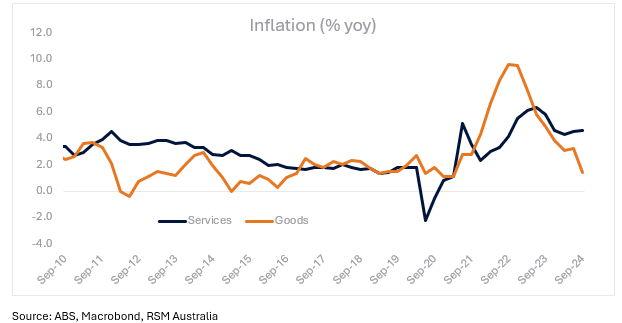

While headline inflation has eased, primarily due to fiscal subsidies and falling fuel costs, core inflation remains stubbornly high at 3.5% as of Q3 2024. The RBA is focused on sustained reductions in core price pressures, with political risks—such as a potential stimulatory pre-election budget in early 2025—adding complexity to its policy path.

Economic growth is likely to remain tepid, buoyed by public spending until private consumption revives. Households face persistent challenges with limited spending power. While wage growth and tax relief provide modest support, most disposable income is being funnelled into rebuilding savings, delaying a broader recovery in consumption. This creates a challenging environment for businesses, which are expected to contend with constrained profit margins into the first half of 2025.

The labour market, which achieved record job growth in 2024, has demonstrated unexpected resilience. Tighter immigration policies, combined with businesses adopting productivity-enhancing technologies and upskilling initiatives, may drive short-term productivity gains in 2025. However, the long-term outlook is more concerning. Stricter immigration measures risk curbing services exports and worsening Australia's skilled labour shortages, a challenge already intensified by an ageing population.

Trade and industry performance remain critical to recovery. While commodities exports anchor the economy, volatility in coal and iron ore prices exposes Australia to global risks. Investments in renewable energy and sustainability are growing in response to climate-related challenges, but stricter lending standards linked to sustainable practices may complicate access to finance.

On the global front, Trump 2.0 introduces uncertainty. While Australia’s trade deficit with the U.S. shields it from immediate tariff risks, escalating U.S.-China trade tensions could have ripple effects. A weakened Chinese economy—Australia's largest trading partner—would dampen demand for Australian commodities, significantly impacting external sector revenues. Retaliatory trade measures or increased competition from cheap Chinese imports could further strain local producers. However, we do not expect these risks for Australia to materialise before the second half of 2025.

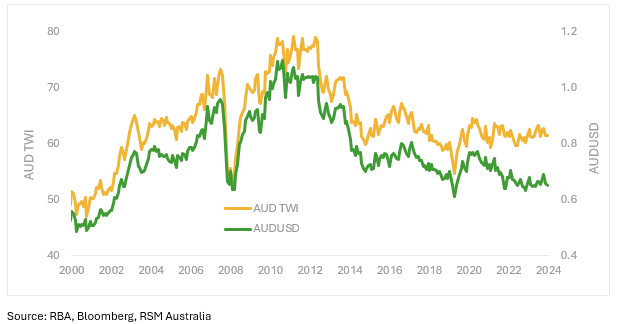

In the near term, the outperformance of the U.S. economy presents both opportunities and challenges. Increased demand for Australian commodities and investment flows could boost growth, but higher global interest rates, driven by robust U.S. economic performance, would tighten financial conditions locally. A stronger U.S. dollar, while making Australian exports more competitive, could also raise import costs and fuel inflation.

All in all, the RBA faces a delicate balancing act. While some economic indicators hint at room for a less restrictive policy, there aren't enough reasons to pivot just yet. Any rate cuts will be limited, with a terminal rate of 3.35% anticipated by the end of 2025. Balancing these domestic and global challenges will require a steady hand.

Australian businesses are facing a perfect storm of challenges that threaten their stability and long-term viability.

Consumer Demand and the Rising Tide of Insolvencies

Tax Holiday Aftermath and ATO Crackdown

The Persistence of Zombie Companies

Economic Uncertainty Undermining Confidence

The Construction Sector's Unique Struggles

Regional Variations in Business Challenges

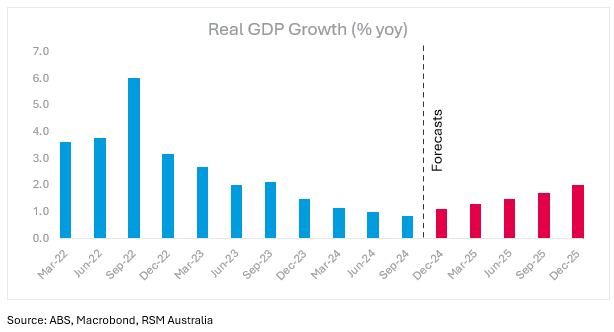

We expect a rather slow pace of pick-up in economic activity despite sizeable government spending as private consumption remains modest. We remain bearish in our outlook and expect the economic recovery to be gradual and drawn out. The imminent fall in population growth as stricter migration policies gain traction and the evident expiry of government support means the onus is on private sector demand to keep the economy afloat.

Our baseline forecasts for the economy show activity picking up to 1.1% yoy in 4Q24 followed by average annual growth of 1.8% in 2025, peaking at 2.0% yoy in 4Q25.

Despite a sharp fall in discretionary spending for most of 2023 and 2024, household consumption is expected to pick up in the new year. Prominent banks have been reporting that the spare cash from tax cuts and fiscal subsidies is currently being saved. This is further evidenced by a pick-up in household savings ratio to 3.2% in 3Q24. The September quarter also saw gross disposable incomes rise 1.5% led by tax cuts while household spending languished at 0.6%. A high-interest rate environment means households have been receiving handsome interest on their savings and offset accounts which are partly offsetting the interest paid on dwellings.

We believe as the Reserve Bank of Australia finally begins easing in 2025, the financial strain on mortgage holders will reduce further and the freshly built savings buffer will further encourage spending. Businesses should expect a pick-up in activity from the second half of 2025 requiring increased investment on their part, further supporting the economy.

Public sector demand surged in the third quarter of 2024, fuelled by robust investment growth and steady increases in public consumption. This trend reinforces our view that the public sector - particularly the care economy - will remain a key driver of broader economic expansion.

Looking at industry performance, we expect mining to continue to be a drag among non-financial corporations. After falling for the third consecutive quarter in 3Q24 by 9.1%, we expect the sector to continue its weak run in 2025 as Australia remains exposed to the risk of falling commodity prices due to weaker global demand, particularly from China. On a positive note, financial corporations are likely to extend their robust performance into the first half of 2025 as a high-interest rate environment drives growth in loan and deposit balances.

The labour market is expected to loosen in 2025. We expect the unemployment rate to average 4.5% in the new year with a gradual pick up in the jobless rate beginning 1Q25 at 4.3%.

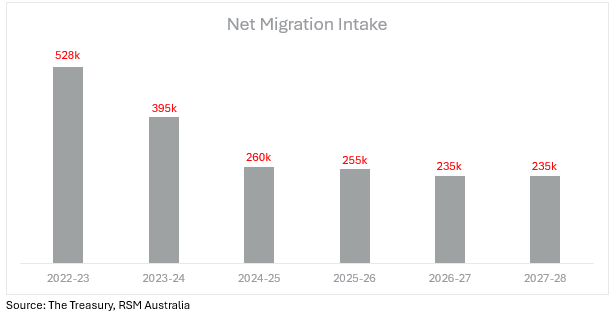

The government has capped the next financial year’s Permanent Migration Programme at 185,000 places, with 70% (132,200 places) allocated to the Skill stream. This represents a reduction from the 190,000 places set for 2023–24, narrowing the focus on applicants meeting Australia’s long-term skill requirements. From 2025–26, the government will extend the planning horizon for the Migration Program from one year to four years, aiming to foster a more strategic and efficient migration system through the ongoing Migration Strategy reforms. Net overseas migration is expected to decline by 110,000 individuals starting 1 July 2024, with forecasts projecting a nearly 50% drop from 528,000 in 2022–23 to 260,000 in 2024–25.

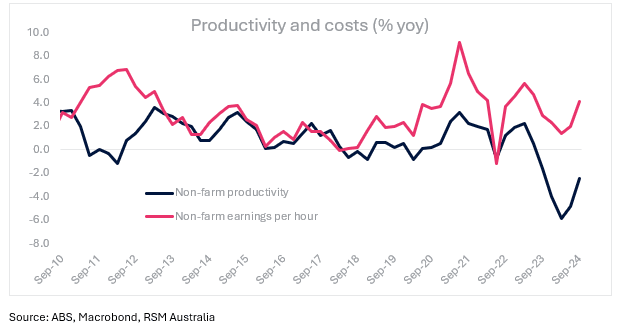

Migration is essential for addressing skill gaps and sustaining workforce growth, particularly in industries that depend on both low - and highly skilled labour. Without migrants, Australia risks a shrinking workforce due to its ageing population, exacerbating structural unemployment and skill mismatches, which are already major concerns for businesses. We believe recent robust job growth may reflect businesses hiring to offset poor productivity rather than indicating a genuinely tight labour market.

Restricting migration might boost productivity in the short to medium term by forcing businesses to optimize their existing workforce. However, in the long run, it will intensify skill shortages, likely hinder overall productivity, and reduce economic output. A smaller pool of workers will likely increase competition, driving up wages in some sectors while worsening shortages in others – an episode we have seen just as Australia got out of the pandemic. We expect wages to inch up as migrant arrivals moderate. It is highly unlikely that wages growth, much like policy rates will revert to their pre-pandemic levels in the long term. This imbalance risks driving inflation, particularly in industries like healthcare, agriculture, and construction, where migrant contributions are indispensable.

For businesses, especially in regional areas, these dynamics may lead to higher labour costs, reduced competitiveness, and stagnation in economic growth.

The Reserve Bank of Australia (RBA) could face contrasting pressures on its monetary policy stance. Slower population growth and subdued consumption could weigh on domestic demand, while persistent government spending strains fiscal resources. Combined with geopolitical uncertainty and rising labour costs due to a constrained workforce, private investment may falter, further dampening economic activity. If these conditions persist, the RBA may be compelled to cut rates sooner to stimulate demand, support private investment, and stabilize employment levels, particularly if the economic slowdown undermines confidence and growth prospects. In this case, we expect an early pivot to less restrictive rates penciling in the first cut to come in 1Q25. Given the early start to the easing cycle, we expect 25 basis points cuts in each of the four quarters of 2025.

Conversely, global factors such as U.S. economic outperformance and a trade war between the U.S. and China could exacerbate Australia's challenges. Capital outflows, driven by higher returns in the U.S., may weaken the Australian dollar, while deflationary pressures from an influx of cheap Chinese goods complicate domestic pricing dynamics. At the same time, reduced demand for Australian exports could amplify downward pressure on the currency, importing inflationary risks. These factors might push the RBA to delay rate cuts, as the balance between controlling imported inflation and supporting growth becomes increasingly precarious. That said, the risk then is for rate cuts to commence by the second quarter of 2025, with the first reduction likely to be a more moderate 25 basis points. Similar cuts are expected in the third and fourth quarters, bringing the terminal rate to 3.60% by the end of 2025.

The timing of monetary policy adjustments will hinge on how these opposing forces evolve and interact with domestic economic conditions.

Devika Shivadekar

Devika Shivadekar is an Economist for RSM Australia based in our Sydney office.

She has a wealth of experience in macro-economic and financial research, spanning both public and private sectors, and a deep understanding of the APAC region. She follows key macroeconomic indicators such as growth, inflation, central bank decisions and the labour market to assess the overall health of an economy.