The enactment in April 2024 of the Treasury Laws Amendment (Foreign Investment) Act 2024 (Cth) (Foreign Investment Act), with purported retrospective application, has failed to avert mounting and substantial claims for the refund of ‘discriminatory’ surcharges imposed by the various states and territories on foreign buyers and owners of Australian real property.

Residents of impacted countries who have paid foreign surcharges in connection with the purchase and/or ownership of real property in Australia are encouraged to consider their options, given the material refunds to which they may be entitled.

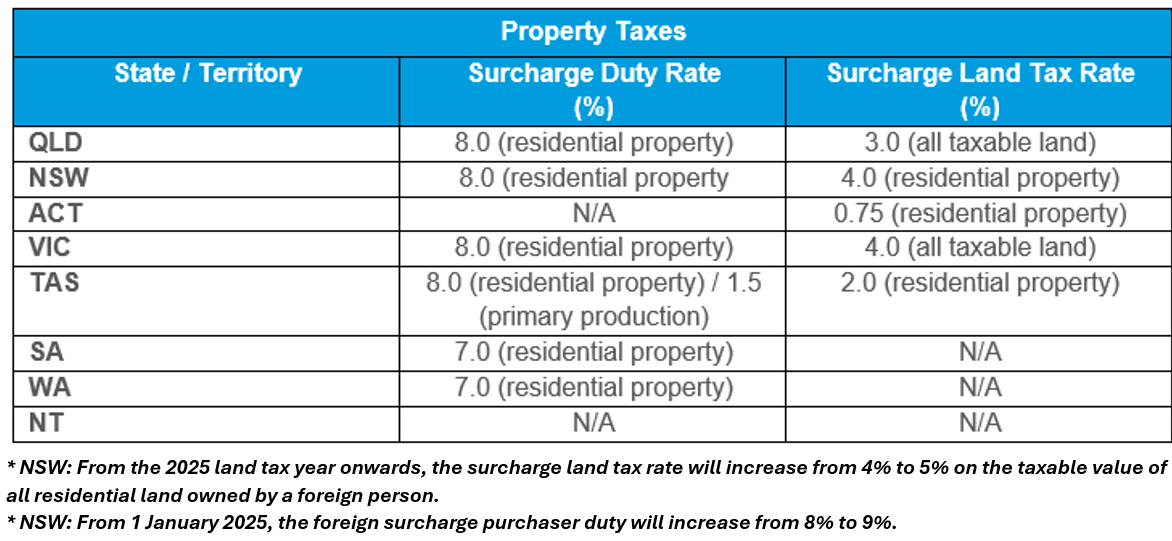

Foreign Surcharges

All Australian states as well as the ACT impose higher costs on foreign buyers and owners of residential property in the form of either one or both of foreign surcharge purchase duty or foreign surcharge land tax – in some states those foreign surcharges extend to non-residential real property. The following table sets out the state of play across the various states and territories:

Issue

Of the more than 40 Double Tax Agreements (DTA) that Australia has with various jurisdictions globally, those with the following countries contain non-discrimination articles that extend to all forms of ‘tax’ (e.g., state or territory-based imposts):

- Finland;

- Germany;

- India;

- Japan;

- New Zealand;

- Norway;

- South Africa; and

- Switzerland.

Those non-discrimination clauses essentially obligate both treaty partners to ensure parity between nationals of both countries from a tax standpoint where the same circumstances apply.

Relevantly, Australia’s DTAs are given legal effect by the International Tax Agreements Act 1953 (Cth) (Agreements Act), a Commonwealth law, whereas section 109 of the Commonwealth of Australia Constitution Act 1901 provides for Commonwealth law to prevail over state or territory law in the event and to the extent of any inconsistency.

Revenue NSW was first alerted to the incompatibility of foreign surcharges (regarded as a tax) with the Agreements Act on or around July 2022 upon receipt of a foreign surcharge purchaser duty objection. Whereas Revenue NSW thereafter exempted nationals of the abovementioned eight countries from foreign surcharges and offered refunds of foreign surcharges paid, though limited to surcharges paid on or after 1 January 2021, other revenue authorities such as the Queensland Revenue Office and Victorian State Revenue Office steadfastly rejected such applications.

Foreign Investment Act

In response to the ensuing chaos, the Foreign Investment Act was instituted. The Foreign Investment Act achieves its stated object of ‘[resolving] any inconsistencies between the Agreements Act … and laws imposing taxes … other than [income tax or fringe benefits tax2]’ through an express ordering rule whereunder domestic laws imposing any tax other than income tax of fringe benefits tax prevail in the event of any inconsistency with the provisions of Australia’s DTAs.

The Foreign Investment Act is stated to apply retrospectively in relation to covered taxes that are payable:

On or after 1 January 2018; and

In relation to tax periods (however described) that end on or after 1 January 2018.

The retrospective period broadly aligns with the statute of limitation periods generally provided under state and territory legislation.

Reception

There has been much disquiet in response to the enactment of the Foreign Investment Act, in particular its purported retrospective application. A class action is already underway against the Victorian Government seeking restitution of up to $500 million3 and a similar class action against the Queensland Government under consideration. Litigation funder CASL is expected to underwrite both class actions.

In light of these developments, nationals of the eight specified countries who have paid foreign surcharges in connection with the purchase and/or ownership of real property in Australia should consider their position and potential entitlements, which may be significant given that foreign surcharges were introduced in some states (e.g., Victoria) as early as 1 July 2015 and in NSW on 1 July 2016.

With respect to NSW, this insight is relevant to individuals from the above-mentioned countries that have paid surcharge land tax or surcharge purchaser duty in NSW on or after the introduction date of 1 July 2016 but before 8 April 2024.

FOR MORE INFORMATION

If you would like to discuss the potential application of these developments to your circumstances, or any other state tax matter, please contact Mira Brewster, who is RSM Australia’s State Tax Specialist.

- Northern Territory does not impose foreign surcharges.

- Agreements Act, subsection 3(1).

- Foreign Purchaser Surcharges Class Action – Register Now (fpsclassaction.com.au)