Acquiring a company is a complex endeavour, often involving significant financial and strategic considerations. A common challenge faced by investors is that target companies are not necessarily audited and unwilling to undergo a full audit before acquisition. While the absence of audited financial information may pose significant risks, it need not be a deal-breaker.

Understanding the Risks

When dealing with unaudited targets, investors may face a range of potential risks, including:

- Financial inaccuracies: Without a rigorous audit, there is a higher chance of inaccurate or incomplete financial information.

- Unrecognised liabilities: Unrecognised liabilities, contingent liabilities, or legal issues could surface post-acquisition.

- Compliance issues: Undetected compliance breaches could negatively impact the value or operations of the acquired business.

Mitigating Risks through Thorough Due Diligence

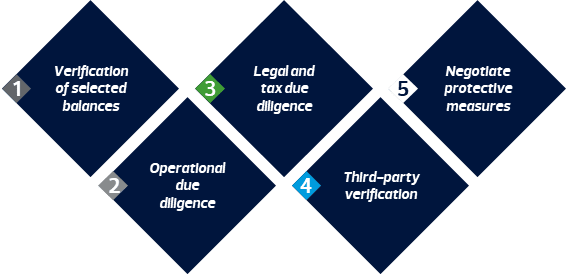

While an audit provides a comprehensive assessment of a company’s financial performance, financial position, and compliance with financial reporting standards, alternative approaches can help mitigate risks associated with unaudited targets:

Verification of Selected Balances – beyond conventional financial due diligence scope of work, acquirers can consider:

- Verification of profit or loss items: Undertaking procedures to verify the accuracy, completeness, and validity of balances, including but not limited to revenue and selected expenditures. This may extend to the conversion of revenue to cash, or expenses to payments.

- Verification of bank statements: Examine bank statements and bank reconciliations to verify cash balances and identify any unusual transactions or discrepancies.

- Assessment of accounts receivable and payable: Review aging schedules and customer/supplier contracts to assess the quality of the target's receivables and payables, including the collectability of receivables or payment cycles of the payables.

Analyse inventory: Verify inventory levels, assess valuation methods, and identify obsolescence risks, either through inventory count observations, or through ageing reports.

Operational Due Diligence:

- Evaluate management team: Assess the experience, qualifications, and integrity of the target’s management team.

- Review key contracts: Analyse contracts with customers, suppliers, and employees to identify any potential risks or liabilities.

- Assess operational processes: Evaluate the target's operational processes, including the effectiveness of its key controls.

Legal and Tax Due Diligence:

- Review of legal documentation: Analyse contracts, leases, permits, and licenses to identify any legal issues or compliance risks.

- Assess tax compliance: Review tax returns and filings to ensure compliance with tax laws and regulations.

Third-Party Verification:

- Engage specialised experts: Consider hiring industry experts or consultants to provide specialised assessments of specific areas, such as technology, intellectual property, or environmental compliance.

Negotiating Protective Measures:

- Escrow arrangements: Establish escrow accounts to hold a portion of the purchase price until certain conditions, such as the completion of a post-acquisition audit, are satisfied.

- Earn-out provisions: Structure the deal to include earn-out provisions, tying a portion of the purchase price to the target's future performance.

- Representations and warranties: Negotiate strong representations and warranties from the seller to safeguard against undisclosed liabilities or misrepresentations.

By adopting a comprehensive due diligence approach and leveraging the expertise of experienced professionals, investors can make informed decisions and mitigate risks when acquiring unaudited targets.