Key takeaways

The ORSA, beyond its regulatory aspect, is an essential tool for understanding the company’s environment, optimizing capital, and making strategic decisions. In an environment where risks are constantly increasing, this article details one of the levers for exploiting this mechanism to its full potential.

A Key Tool for Sustainability

Since its first application nearly 10 years ago, the ORSA has played a vital role in bridging political-strategic decisions with their operational implementation. Beyond the technical and organizational aspects, the internal risk assessment mechanism that accompanies it connects key players, including at least: the top executives, heads of key functions, political bodies, supervisors, and others.

A Constant Challenge in an Evolving Risk Environment

However, the ORSA continues to challenge stakeholders in the insurance market. The cross-cutting nature of the mechanism, the number of involved parties, and the demanding work contribute to its complexity, which is constantly intersected by the evolving company environment, whether regulatory, technological, economic, social, or ecological. The ORSA constantly requires a reassessment of risks tied to major crises events influencing the assessment of insurance risks, such as: the COVID-19 pandemic, the sudden rise in inflation and its impact on interest rates, worsening climate-related claims, or cybercrime and its many associated operational risks.

A Management Tool

In line with the directive, the ORSA is a critical management and measurement tool essential for ensuring the long-term stability of insurers. This tool offers several useful features, including justifying strategy through “stress tests” and the ability to maintain development capacity by wisely investing in tools and financial solutions available on the market. Regardless of the chosen option, optimization relies on rigorous risk management.

Relying on the Experience of Key Functions

The second pillar of Solvency II has structured, focused, and formalized the risk monitoring of each insurance sector player. The risk mapping provides a wealth of information that should be leveraged to assess its full impact on the ORSA. The value of this approach is not only to identify and manage risks but also to align the company’s strategies with its solvency capacity.

How Many Companies Can Connect Their Mapping to the ORSA?

Operational Risk as an Optimization Lever

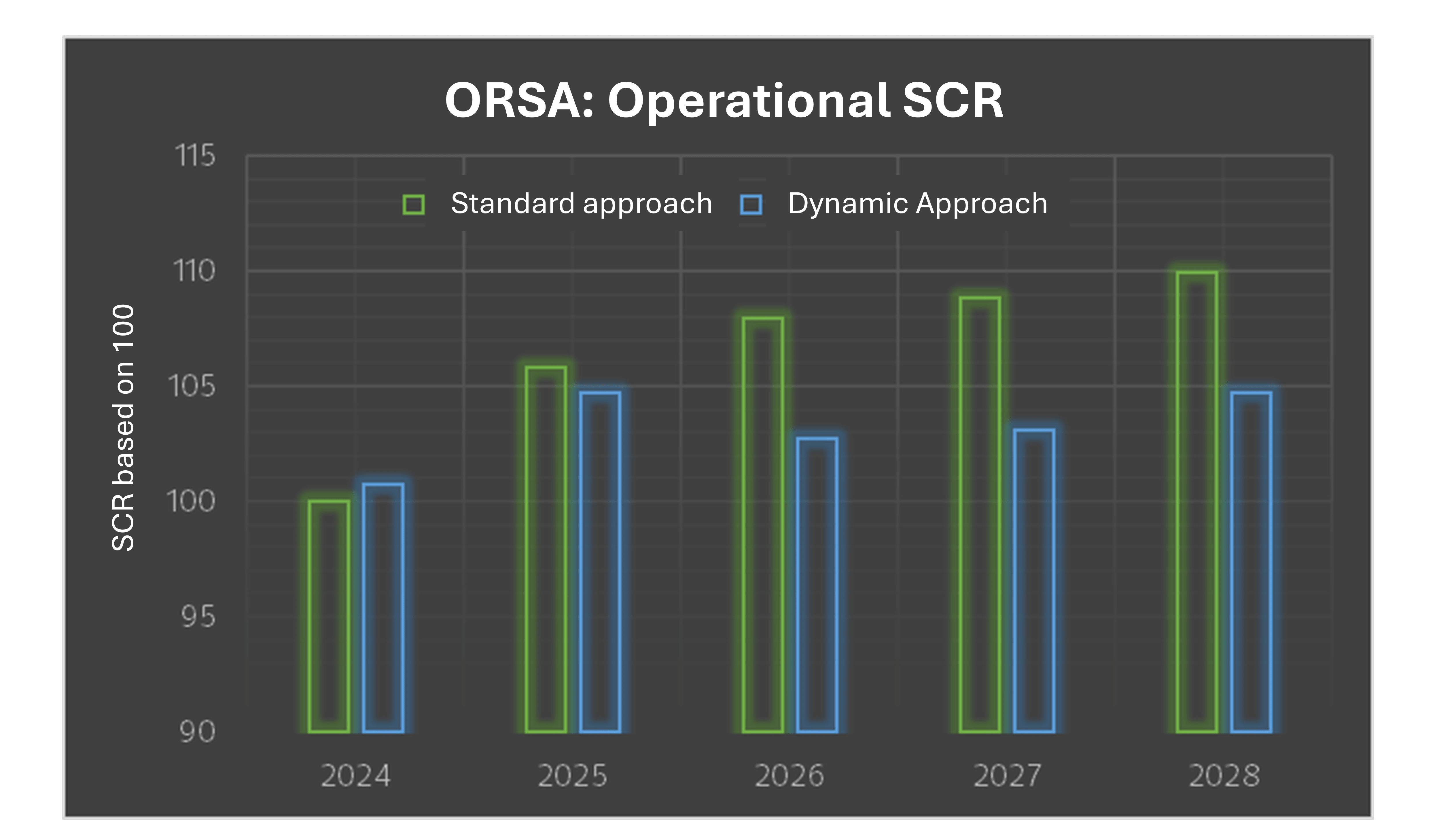

The capital add-on for operational risk is one such optimization lever, but its assessment is not always the easiest. While the standard formula helps most companies calibrate the necessary prudential capital to cover this risk, the ORSA is a very different exercise for insurers, as it requires rethinking the parameters and adapting them within a prospective environment, ensuring business continuity.

Dynamically Assessing Operational Risk

Thus, the optimal approach to evaluating operational risks for an insurance company relies not only on a thorough understanding of the specific vulnerabilities of its management systems, subcontractor risk management, reputation, or human resources but also on its ability to assess all of these main risks in the medium term. To achieve this, a precise assessment of the operational SCR through a “dynamic” risk approach is a way to better manage the use of economic equity to support the company’s development. Indeed, all stakeholders agree that operational risks can emerge, evolve according to mitigation measures taken by the company, and eventually disappear for some.

Dynamic Risk in the Service of the Global Solvency Requirement

What about reputational risk or the cost of renewing an IT infrastructure? The dynamic ORSA approach, especially when evaluating the global solvency requirement of clients, is based on a series of inquiries. It relies on:

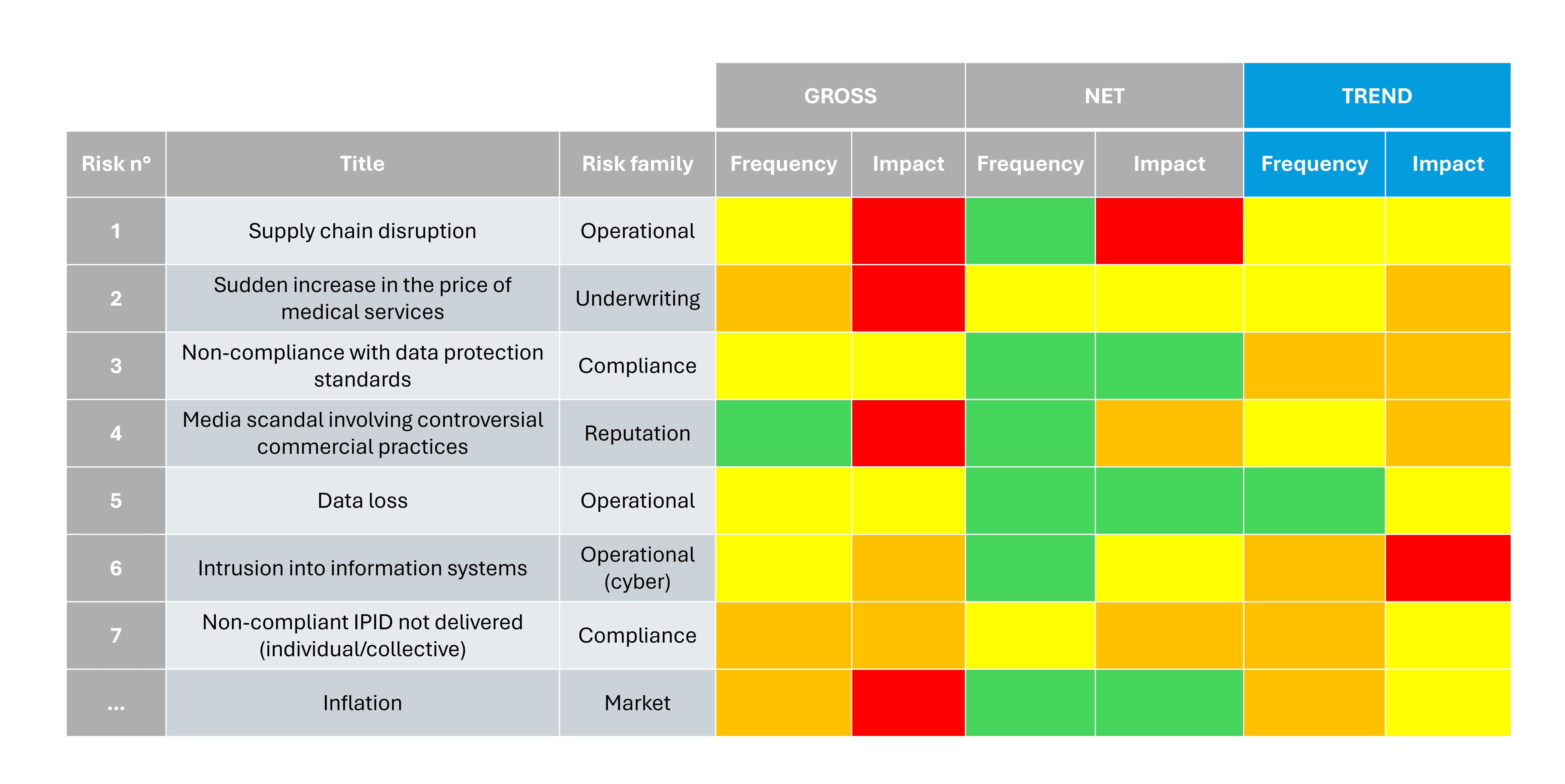

- A double identification of risks (based on criteria of intensity, frequency, and also trends):

- Top-down, to capture how the impact of realized major risks identified by governance unfolds within the company;

- Bottom-up, relying in particular on the risk map established by internal control, viewed through the lens of Solvency II, to obtain a more “technical” vision of major risks, going beyond governance’s perception.

- A prudential vision of the entire evaluation process: identified risks are classified into coherent sub-modules and then integrated into the BSCR using a correlational approach.

This approach, already deployed among our clients, complements many other levers for optimizing and developing capital, such as activity diversification, customer retention, or expanding distribution networks...

Our dedicated Actuarial team is available to assist and advise you in a constantly evolving prudential and regulatory environment, helping you manage all your exposures and forecasts related to accounting, technical, and financial risks.

Discover our Actuarial services.