Indonesia, as one of the world's largest gold producers, contributes approximately 4% of the global supply.

However, inefficiencies in the domestic bullion trade continue to hinder its full potential. Dependence on international intermediaries, high transaction costs, and regulatory gaps limit the country’s ability to fully capitalize on its bullion reserves. To address these challenges, the Indonesian government is exploring the establishment of a bullion bank to facilitate storage, trading, and financing activities. This initiative mirrors global trends, where bullion banking services enhance market efficiency, transparency, and accessibility in the precious metals sector.

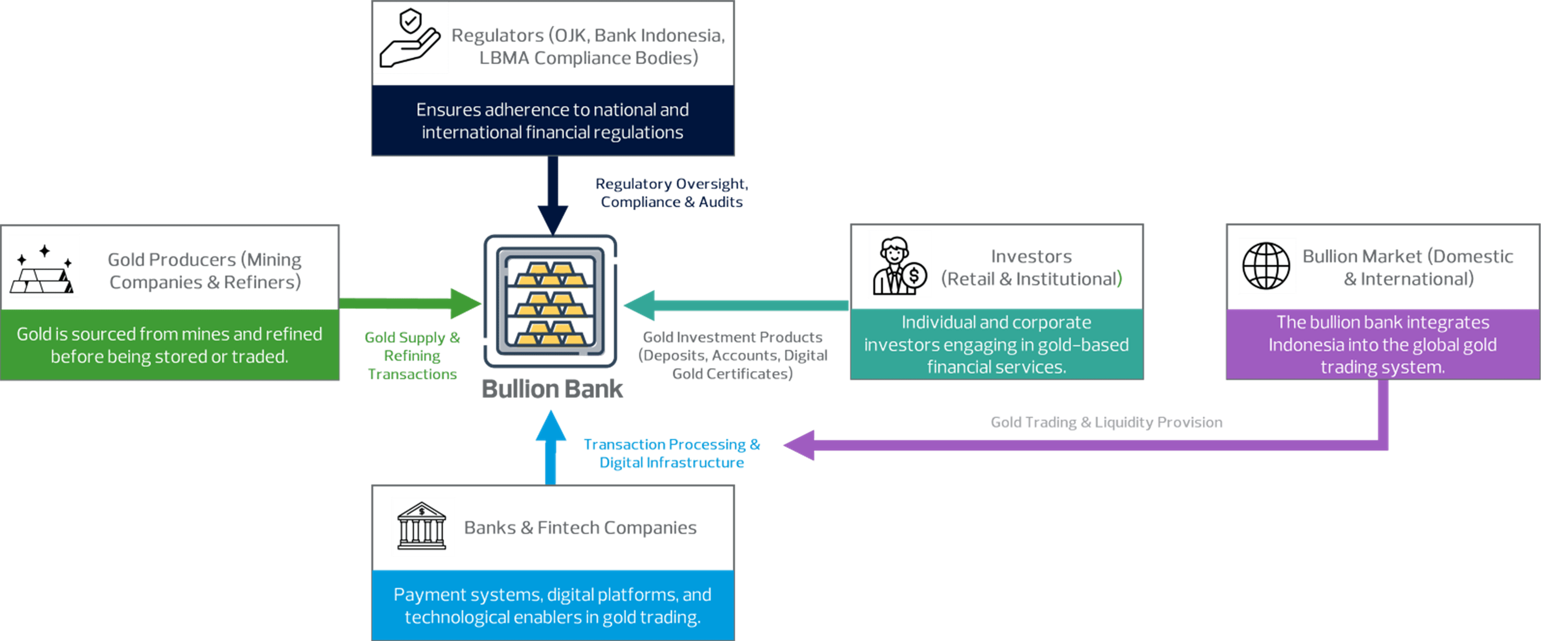

A bullion bank would create a structured domestic gold market, reducing reliance on foreign trading hubs while ensuring transactions comply with London Bullion Market Association (LBMA) standards. Enhanced liquidity and transparency would promote financial inclusion, allowing broader participation in gold markets. By certifying and processing bullion domestically, Indonesia could capture more value from its gold production, reducing raw exports and strengthening its global market position.

Regulatory Framework and Governance

A well-defined regulatory framework is fundamental to ensuring the stability and security of a bullion bank.

Supervision by Otoritas Jasa Keuangan (OJK) and Bank Indonesia (BI) would ensure investor protection and transaction integrity. Tax policies and investment incentives should be structured to attract capital while maintaining a fair and competitive market environment.

Adopting LBMA Good Delivery standards would enhance credibility, allowing Indonesia’s bullion market to integrate with global financial systems. Additionally, Regulatory Technology (RegTech) could automate compliance monitoring, reducing risks related to fraud and financial crime. Independent audits would reinforce transparency, strengthening investor confidence in bullion banking operations.

Technology Adoption and Security Considerations

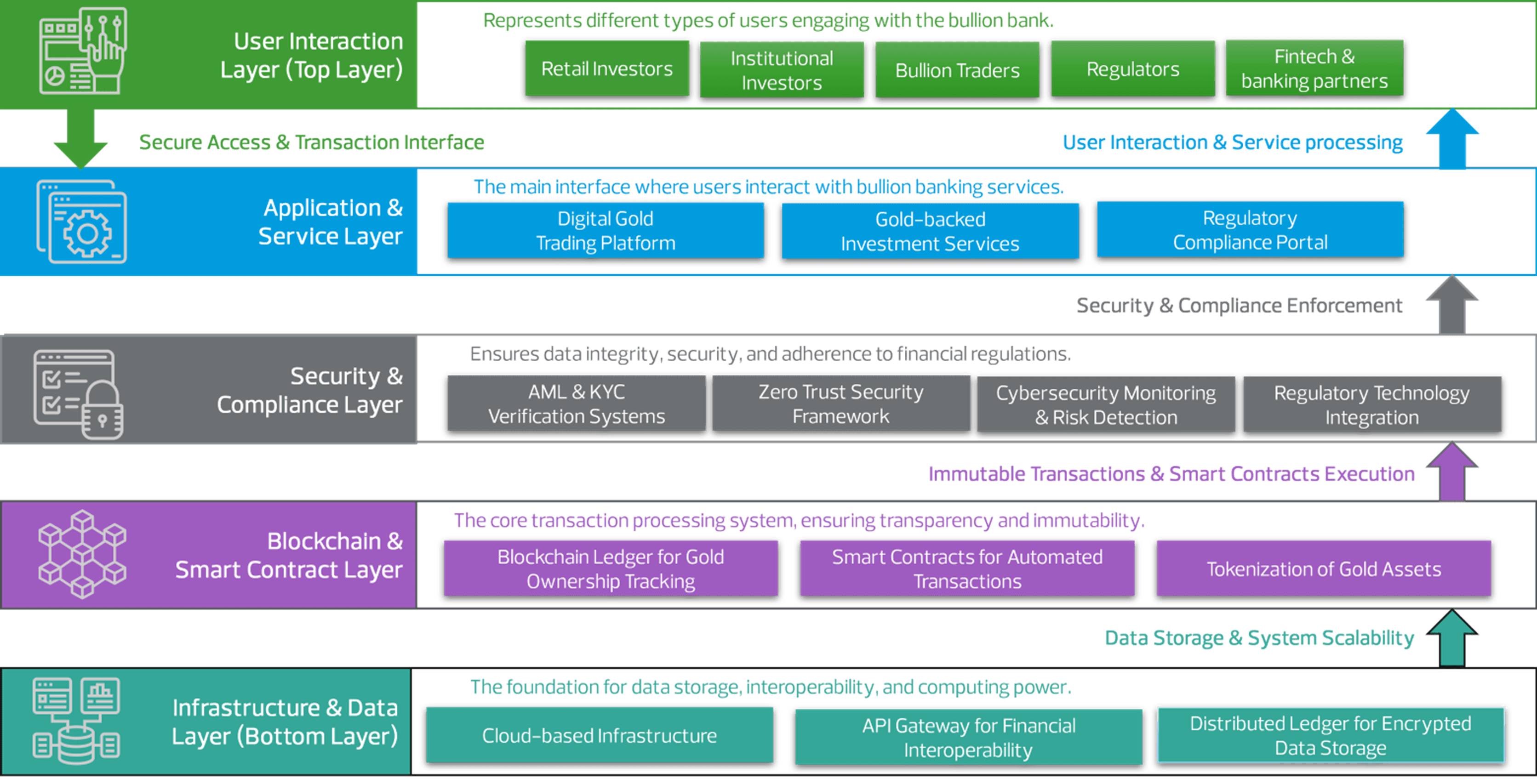

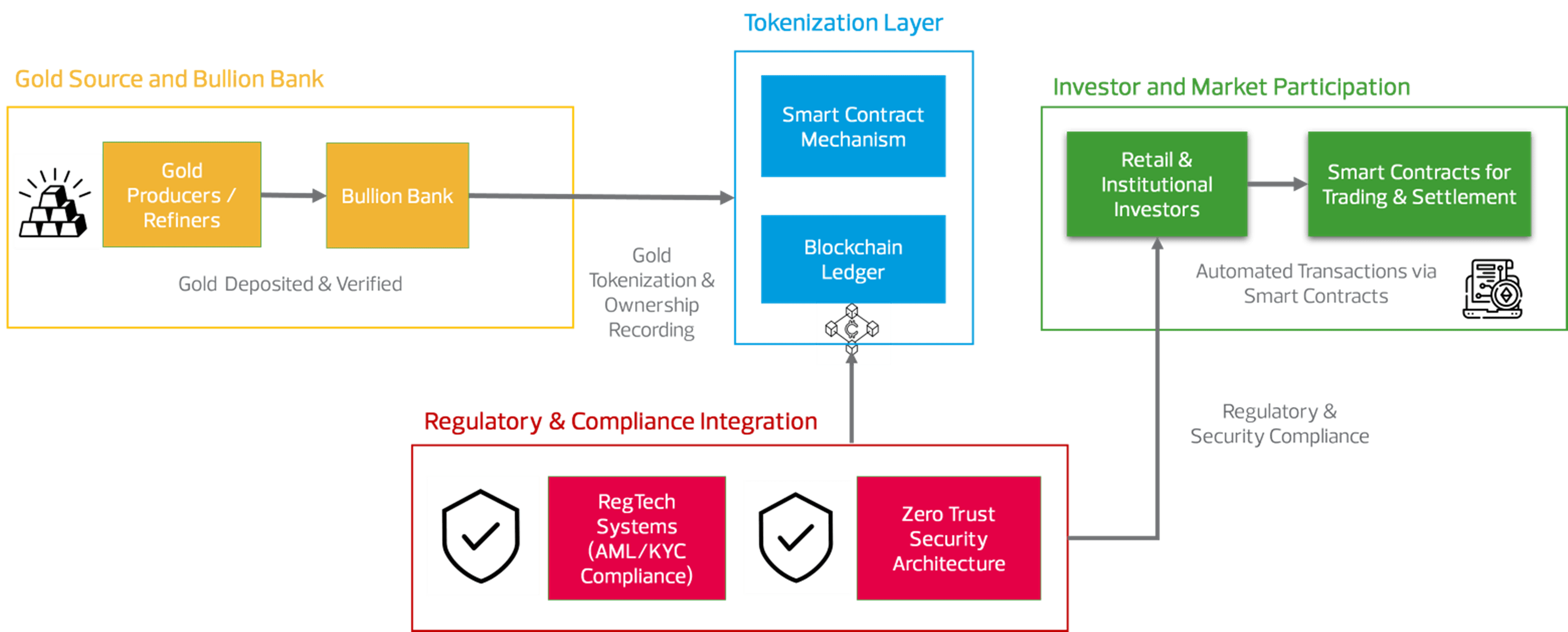

The success of a bullion bank hinges on cutting-edge technology integration. Blockchain technology would ensure transparency by maintaining immutable ownership records, mitigating risks of fraud and counterfeiting. Artificial intelligence (AI) and machine learning could strengthen risk management by detecting suspicious transactions in real time and ensuring adherence to anti-money laundering (AML) and know-your-customer (KYC) regulations.

Given the high-value assets involved, cybersecurity must be a top priority. A Zero Trust Architecture would restrict system access to verified users, preventing unauthorized transactions. Distributed ledger technology would enable encrypted storage solutions, safeguarding customer information and bolstering trust in digital bullion transactions.

Technological Infrastructure and Digital Integration

A bullion bank’s technological infrastructure must support advanced security, seamless transactions, and market accessibility. Digital platforms would facilitate real-time trading, secure storage, and bullion-linked financial transactions. Blockchain-based tokenization of gold assets would allow fractional ownership, broadening investor participation and enhancing liquidity.

Smart contracts would automate trade settlements, collateralized lending, and interest calculations on gold-backed financial products, improving efficiency and reducing operational risks. AI-driven analytics would enhance fraud detection, anomaly tracking, and regulatory compliance, ensuring secure and compliant transactions.

Cybersecurity must be a priority in digital bullion banking operations. The implementation of Zero Trust Architecture (ZTA) would enforce strict access controls, while distributed ledger technology would secure digital assets and protect against cyber threats.

Interoperability between banking institutions, fintech companies, and regulatory agencies will be critical for a well-functioning bullion banking ecosystem. An API-driven financial framework would facilitate seamless data sharing, compliance tracking, and transaction validation, reinforcing Indonesia’s role as a competitive global bullion hub.

As financial technology evolves, adopting a cloud-based infrastructure would ensure scalability, cost-effectiveness, and enhanced disaster recovery capabilities. Cloud solutions would enable real-time market data access, supporting informed decision-making for investors, regulators, and financial institutions alike.

CONCLUSION

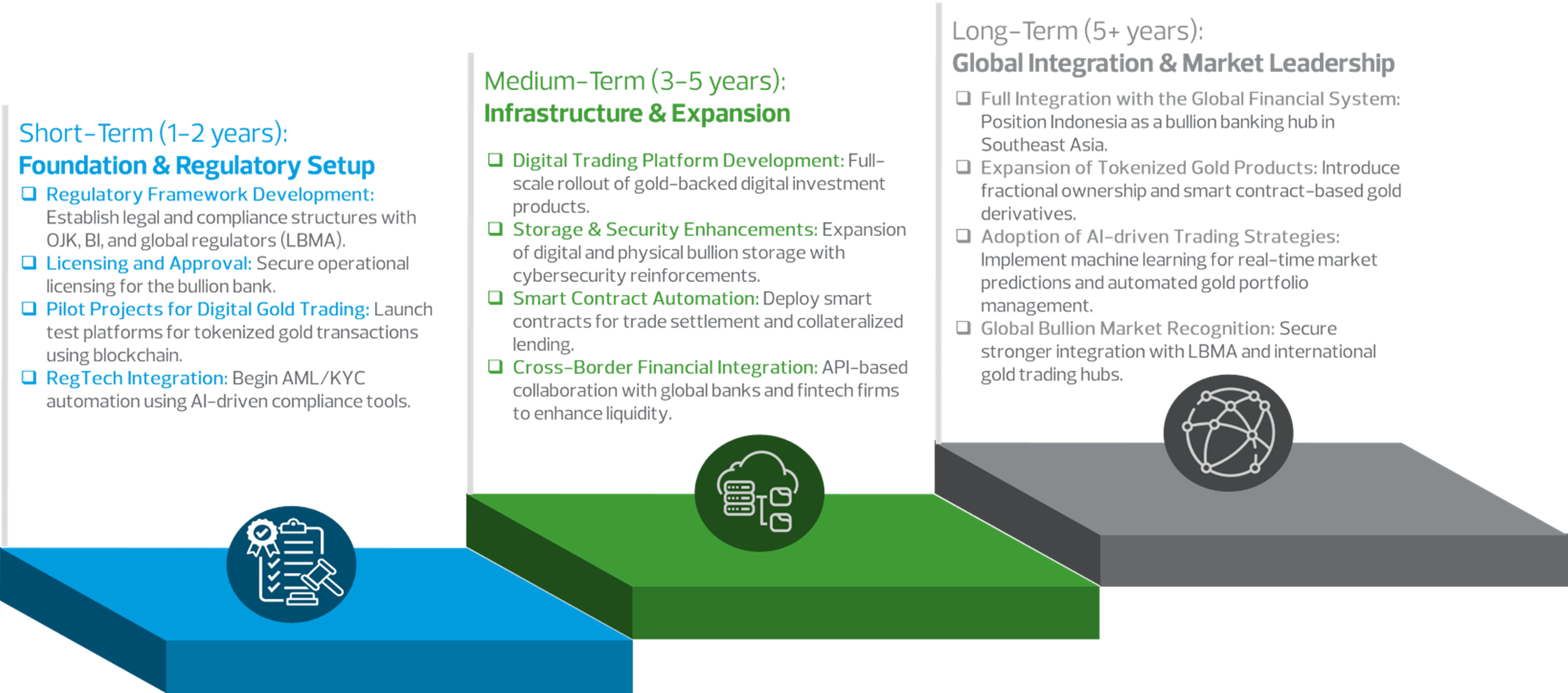

The establishment of a bullion bank in Indonesia represents a transformative opportunity to modernize the country’s gold market, expand financial accessibility, and strengthen economic resilience. By leveraging blockchain, AI, and RegTech solutions, the bullion bank can offer a secure, transparent, and efficient ecosystem for gold transactions. These innovations would not only streamline domestic gold trading but also elevate Indonesia’s position as a key player in the global bullion financial system.

To realize this vision, it is imperative that government and regulatory bodies implement clear, adaptive policies that foster responsible market participation while ensuring security and compliance with international standards. Strengthening interoperability between financial institutions, fintech players, and regulatory agencies will be crucial in creating a seamless and trusted bullion banking ecosystem. Furthermore, by embracing tokenization and smart contract automation, the system can offer innovative investment products that enhance liquidity and financial inclusion.

By Resdy Benyamin, Technology Consulting Practice