RSM INDONESIA CLIENT ALERT – 30 January 2025

The Global Minimum Tax (GMT), also known as Pillar Two, is a key initiative under the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS), aimed at reducing tax competition among jurisdictions, which has been considered a race to the bottom with diminishing benefits for many countries. The primary objective of GMT is to ensure that large multinational enterprises are subject to

a minimum Effective Tax Rate of 15% in each jurisdiction where they operate or, if not, in their home country.

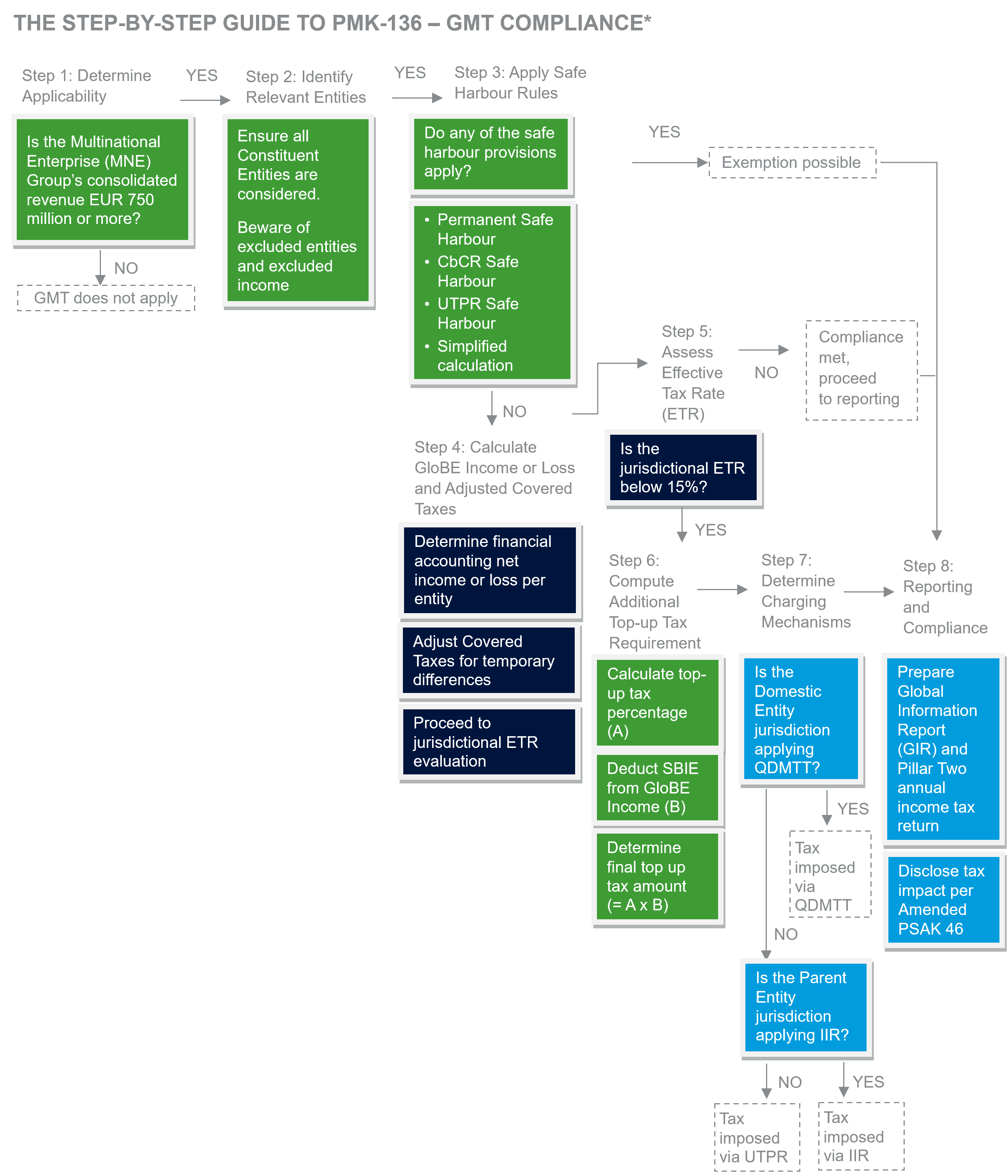

As part of its commitment to the Inclusive Framework agreement reached in October 2021, Indonesia has now implemented GMT through the issuance of Minister of Finance Regulation No. 136 of 2024 (PMK-136), which provides the regulatory framework for the implementation of the Global Anti-Base Erosion (GloBE) Model Rules. The GMT framework applies a 15% minimum tax rate through three key mechanisms: the Qualified Domestic Minimum Top-up Tax (QDMTT), Income Inclusion Rule (IIR), and Undertaxed Payment Rule (UTPR).

WHEN DOES PMK-136 APPLY?

The regulation is effective on 1 January 2025.

REGULATION OVERVIEW

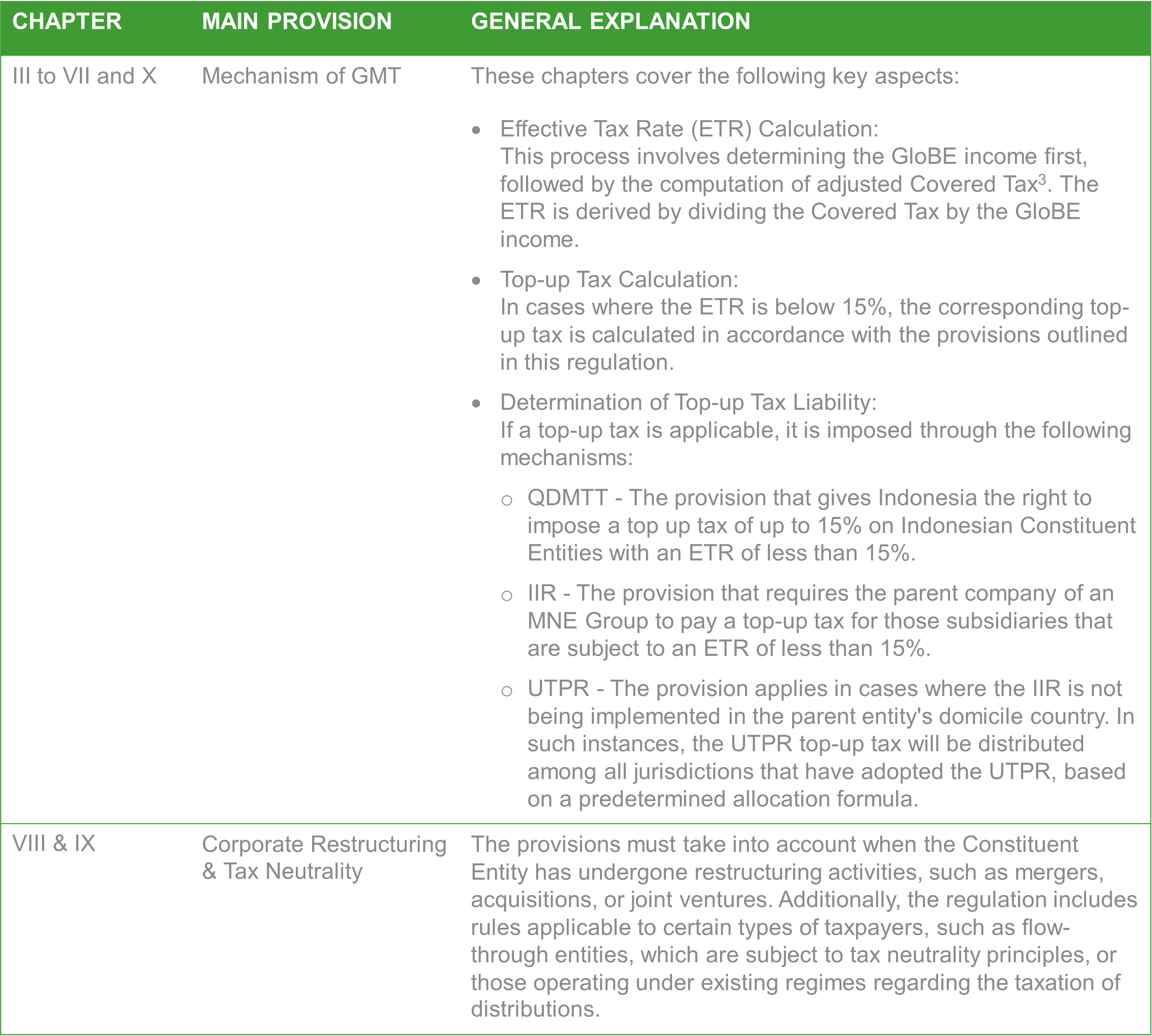

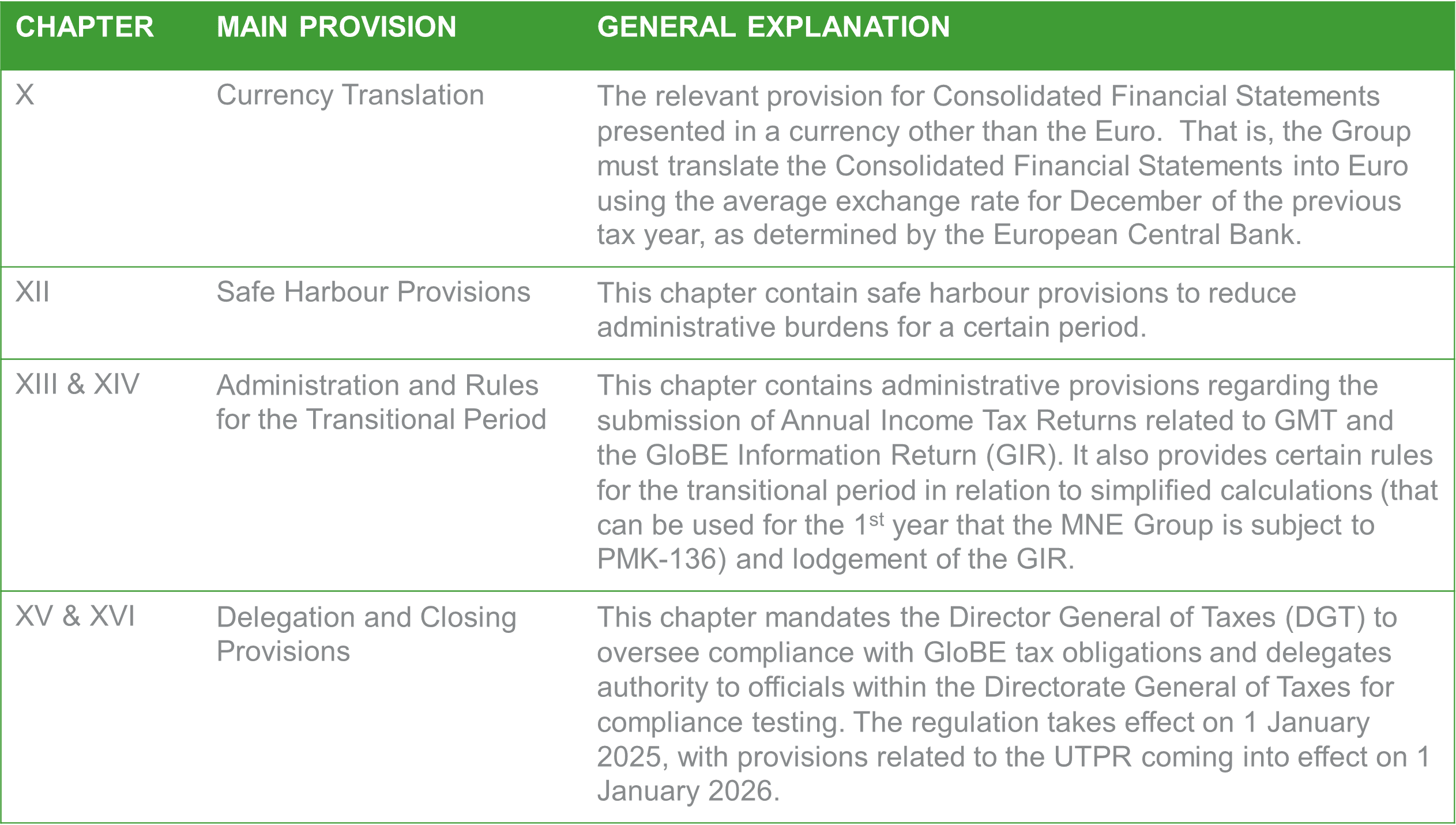

The regulation is complex and spans approximately 200 pages, comprising 15 chapters and 74 articles, including an appendix of more than 100 pages of examples. Chapters I and II outline the general provisions and define the scope of entities subject to the regulation. Chapters III to VII, along with Chapter X, encompass the key operative rules governing the implementation of the provisions. Chapter VIII focuses on matters related to corporate restructuring, while Chapter IX establishes provisions applicable to specific tax neutrality arrangements and existing regimes regarding the taxation of distributions. The regulation also addresses the issue of currency translation in Chapter X. Furthermore, Chapters XII to XIV provide guidelines on safe harbour measures, administrative procedures, and measures for the transitional period. Lastly, Chapters XV and XVI contain provisions regarding the delegation of authority and the closing provisions of the regulation.

The table below summarizes the key provisions outlined in PMK-136.

1A Constituent Entity is defined as every entity that is included within a MNE Group and includes Permanent Establishments.

2The UPE is the entity that has a direct or indirect controlling interest in other entity(ies) within an MNE Group and that parent entity is not controlled by another entity (whether directly or indirectly).

3Covered Tax represents:

MECHANISM OF GMT

a. Effective Tax Rate

To determine whether a top-up tax is required, the process begins with calculating the ETR in each jurisdiction where the MNE Group operates. This involves two fundamental steps: first, determining the GloBE income or loss, and second, calculating the corresponding Adjusted Covered Tax. The ETR is derived by dividing the covered tax by the GloBE income (net profit). That is:

The calculation of GloBE income or loss for a Constituent Entity in a given tax year is primarily based on the net accounting income or loss before consolidation adjustments, using the financial accounting standards applied in preparing the Consolidated Financial Statements of the UPE. To ensure compliance with the GloBE framework, various adjustments as stipulated by this regulation - general, optional, and specific adjustment - must be applied to the financial net accounting income or loss based on the financial accounting standards, enabling consistent and accurate reporting across jurisdictions.

The Adjusted Covered Tax, applicable to GloBE income, includes only income taxes (including Final Tax) while excluding non-income taxes such as indirect taxes, payroll taxes, and property taxes. The regulation also provides specific guidelines for the allocation of withholding taxes related to distributions of profit. The Adjusted Covered Taxes for a tax year represent the current tax expense recorded in the Constituent Entity’s financial statements, incorporating adjustments for additions and reductions in Covered Taxes, deferred tax adjustments, and any changes of Covered Taxes recorded in other comprehensive income.

b. Top up Tax Calculation

Once the ETR has been calculated, taxpayers must determine the amount of additional top-up tax. The applicable additional tax rate is calculated as the difference between the minimum required rate of 15% and the ETR in the respective jurisdiction. This resulting top-up tax rate is then applied to the jurisdiction’s GloBE income, after deducting any substance-based income exclusion (SBIE). The SBIE can be considered as the amount of non-taxable GloBE income, effectively reducing the amount subject to the minimum tax. It is calculated based on a predetermined percentage applied to tangible assets and payroll expenses.

c. Charging Mechanism

(Q)DMTT

PMK-136 introduces a domestic top-up tax designed to align with the GloBE framework, known as the Domestic Minimum Top-up Tax (DMTT). When the DMTT implemented under this regulation meets the requirements set by GloBE rules, it is classified as a “Qualified” Domestic Minimum Top-up Tax (QDMTT), which allows it to offset any potential top-up tax obligations under the GloBE rules applied by other jurisdictions. The introduction of (Q)DMTT reinforces Indonesia’s primary taxing rights over income generated in Indonesia.

IIR

IIR grants Indonesia the right to impose a top up tax on an Indonesian Parent Entity if the jurisdiction where the low-taxed Constituent Entity4 is located does not implement a QDMTT. Under IIR, the top-up tax is levied at the parent entity level, based on its inclusion ratio in the Constituent Entities that have been allocated top-up tax. While the IIR is generally applied at the UPE level, it can also apply to entities further down the ownership structure - such as an Intermediate Parent Entity (IPE) or a Partially Owned Parent Entity (POPE) - if the UPE itself is not subject to IIR.

UTPR

UTPR imposes an additional tax on Constituent Entities in Indonesia that are part of an MNE Group when the low-taxed income of another subsidiary is not taxed through the IIR. The UTPR serves as a safeguard to ensure that the minimum tax of 15% is paid. The tax imposed under UTPR is allocated across jurisdictions based on a substance-based allocation key, which considers factors such as the number of employees and the total tangible assets in the UTPR jurisdictions.

In summary, the top-up tax is applied through the following hierarchy of charging mechanisms:

- The primary right to collect the top-up tax lies with the low-taxed jurisdiction if it has implemented a QDMTT.

- If the low-taxed jurisdiction does not have a QDMTT, the jurisdiction where the UPE is located may impose additional top up tax based on IIR on the income of the low-taxed Constituent Entity.

- If the UPE's jurisdiction does not apply IIR, the top-up tax obligation falls to the next entity in the ownership chain located in a jurisdiction with an IIR, following a top-down approach (e.g., IPE, POPE).

- In cases where the IIR is not applicable, the jurisdictions that have adopted UTPR will collect the top-up tax.

- The tax liability under UTPR is allocated among jurisdictions based on a substance-based allocation method, considering the level of economic activity within each jurisdiction.

d. Safe Harbour

Safe Harbour measures are available for Constituent Entities that meet specific eligibility criteria, enabling them to reduce the additional top-up tax to zero. The measures include the application of simplified calculation methods during a certain period to facilitate the initial implementation phase. Qualifying companies may also leverage readily accessible financial data, such as Country-by-Country Reporting (CbCR).

The Safe Harbour provisions consist of permanent Safe Harbour, CbCR Safe Harbour for a specific period and/or certain entities and groups, UTPR Safe Harbour for a specific period, and simplified calculations Safe Harbour for non-material Constituent Entities.

4A low-taxed Constituent Entity is a Constituent Entity that is located in a jurisdiction where the ETR is less than 15%.

ADMINISTRATION AND REPORTING

UPE of an MNE Group that is considered a domestic taxpayer is required to submit the GIR and a Notification5 to the DGT no later than 15 months after the end of the tax year. However, for the first year of implementation, an extended deadline of 18 months is granted. Therefore, for an MNE Group with a tax year ending on 31 December 2025, the first filing deadline is 30 June 2027.

Constituent Entities that are not the UPE are also required to submit a Notification. The deadline for the Notification follows the timeline of GIR.

In addition, Indonesian Constituent Entities are required to submit the annual income tax returns for Pillar Two, which include:

- the Annual Corporate Income Tax Return for GloBE (if it is a UPE),

- the Annual Corporate Income Tax Return for DMTT for MNE Group members, and

- the Annual Corporate Income Tax Return for UTPR for MNE Group members.

These tax returns must be submitted to the DGT in accordance with the provisions of the Law regarding General Provisions and Procedures of Taxation (UU KUP). Administrative penalties will be imposed for late or inaccurate filings, in line with the applicable regulations under the same law.

A Step-by-Step Guide to PMK-136 compliance is provided at the end of this Client Alert to facilitate an easier understanding of the main provisions of PMK-136.

5The Notification states the identity (including jurisdiction) of the Constituent Entity that will be filing a GIR.

DISCLOSURE OF PILLAR TWO IMPLICATIONS IN FINANCIAL STATEMENTS

If any Indonesian Constituent Entity is part of an MNE Group, then the application of PMK-136 in Indonesia and/or the GloBE rules in other countries might have a financial effect on that entity. Companies affected by Pillar Two, in compliance with IAS 12 and the amendment to PSAK 46 (Income Taxes related to International Tax Reform - Pillar Two Model Rules), are required to separately disclose current tax expenses (or income) related to Pillar Two. The purpose of this disclosure is to provide financial statement users with a clear understanding of the entity's exposure to Pillar Two taxation. The disclosure should include both qualitative and quantitative information, where qualitative details explain the impact of Pillar Two regulations and identify key jurisdictions of potential exposure. Quantitative information should provide insights into the proportion of profits subject to Pillar Two taxation and the applicable ETR, or the potential changes in the entity's ETR when the regulations are enforced.

RSM COMMENTS

It is recommended that companies that are part of a MNE Group undertake the following steps:

Evaluation of Group Structure:

Assess and identify entities within the group that could potentially be subject to additional tax obligations under the GMT framework.

Tax Risk Assessment:

Conduct an analysis to estimate potential additional tax liabilities arising from GMT implementation.

Adjustments to Accounting Systems and Data Point Identification:

Ensure that financial statements align with PSAK 46 requirements for Pillar Two disclosures and comply with IAS 12.

Identify and establish the necessary data points or chart of accounts that will act as the foundation for GMT calculations.

Compliance with Reporting Requirements:

Prepare data required for the GIR reporting.

Compile the annual income tax return along with supporting documentation, such as working papers or Country-by-Country Reporting (CbCR), to maintain compliance with GMT regulations.

Involve both Accounting & Tax Teams:

Given the technical complexity of Pillar Two and its strong connection to accounting principles, it is important to involve the accounting team or advisers in addition to the tax team when assessing the potential implications of PMK-136 and, more broadly, Pillar Two. Strong technical understanding of accounting standards coupled with specialized tax knowledge will facilitate the development and implementation of plans to capture required data, determine tax exposures and accounting disclosures, and file timely income tax returns and GIR.

Consider the implications, especially in relation to an existing tax holiday:

As stated in Minister of Finance Regulation No 69 Year 2024 concerning the Amendment of Regulation No. 130/PMK.010/2020 concerning Provision of Facility for Reduction of Corporate Income Tax (the “Tax Holiday Regulations”), further regulations could be issued to adjust the tax holiday benefit if the relevant entity and its group are subject to GMT. In such cases, PMK-136 may result in an effective reduction to the tax holiday benefit. This may require further regulation, especially for tax holidays granted prior to the issuance of Minister of Finance Regulation No 69. Prudent taxpayers should plan accordingly.

*Disclaimer: This flowchart is developed independently, drawing upon insights from OECD publications, Bloomberg materials, and publicly accessible sources. This document is for informational purposes only and does not represent an official position of any referenced organizations