RSM INDONESIA CLIENT ALERT – 21 June 2024

The new Standards for internal audit has been issued by The Institute of Internal Auditors and will be effective January 2025 and organizations need to prepare for alignment with the new Standards.

BACKGROUND

The International Professional Practices Framework (IPPF) serves as a conceptual framework that organizes authoritative guidance issued by The Institute of Internal Auditors (IIA). As a globally trusted guidance-setting body, the IIA provides internal audit professionals worldwide with essential guidance through the IPPF.

Key points about the IPPF:

- Purpose: It offers required and recommended guidance for internal auditors.

- Guiding Principles: The IPPF emphasizes independence, objectivity, effectiveness, efficiency, and ethical practices.

- Global Standards: The Global Internal Audit Standards (GIAS or Standards) within the IPPF guide professional practice worldwide.

- IIASB Oversight: The International Internal Audit Standards Board (IIASB) continually reviews and updates these standards.

- Recent Updates: In 2023, the IIASB thoroughly reviewed public feedback on draft standards, resulting in updates to the IPPF, including the International Standards for the Professional Practice of Internal Auditing. The new Standards will take effect in January 2025.

The new Standards are not just relevant to internal auditing as it impacts to the entire organization. This means that collaboration is needed to bring implementation of the new Standards to be successful.

APPLICABILITY & STRUCTURE

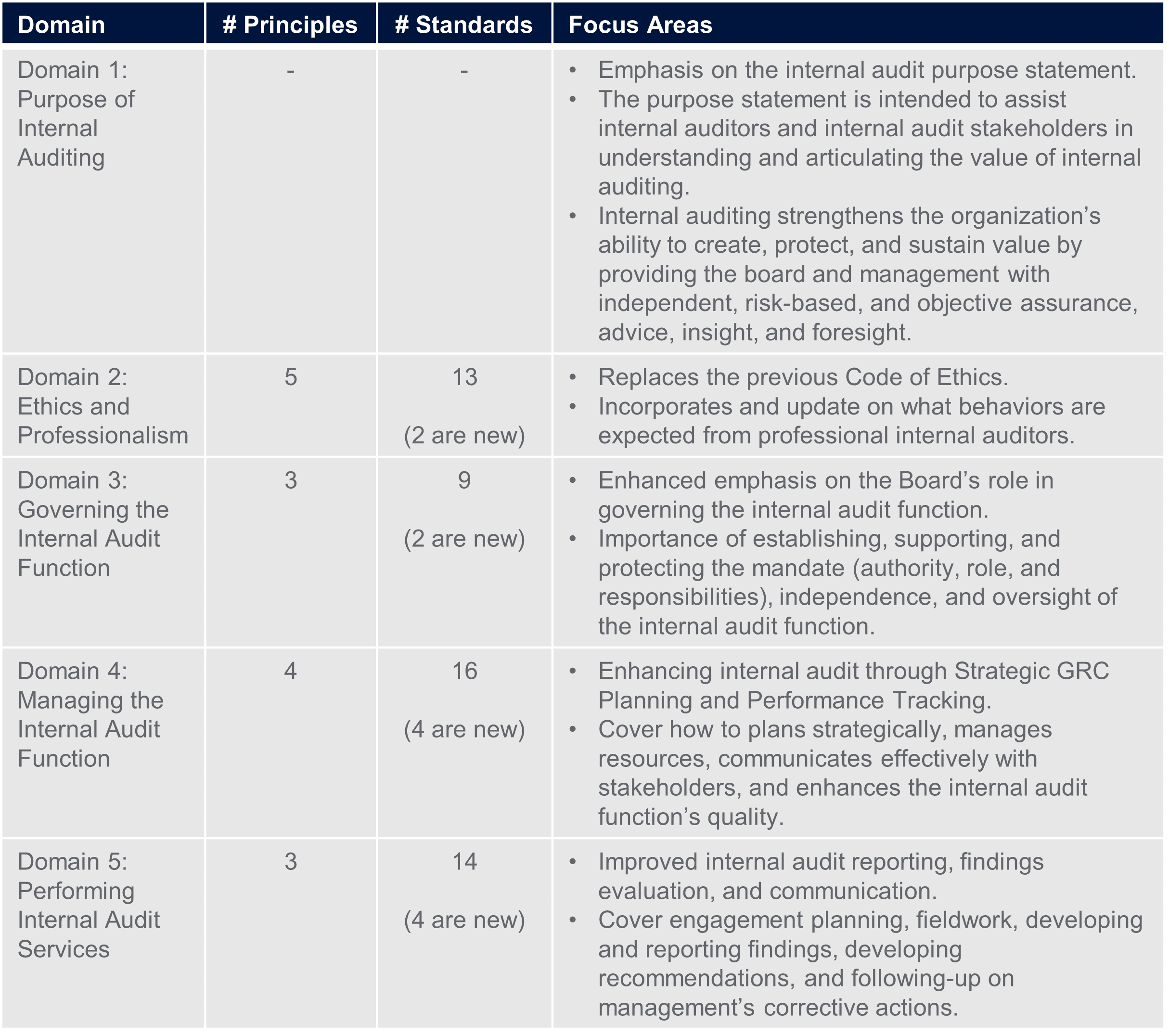

The Standards are principle-focused and provide a framework for performing and promoting internal auditing. It set forth principles, requirements, considerations, and examples of conformance for the professional practice of internal auditing globally. The Standards apply to the internal audit function and individual internal auditors across sectors/industries and size. The Standards are categorized into 5 domains that entails 15 principles and 52 standards.

Structure of the new Standards are more organized, and it greatly relates to enhanced quality of internal auditing and promote continuous improvement.

The need for collaboration among the board, senior management and internal auditing is part of the essential conditions for the governance of internal auditing. The Standards also introduce the concept of Topical Requirements that shall apply when internal auditors are performing engagement on a certain area or topic.

QUALITY ASSESSMENT CONSIDERATIONS

To enhance quality, the Standards describe that Quality is a combined measure of conformance with the Global Internal Audit Standards and the achievement of the internal audit function’s performance objectives. Therefore, a quality assurance and improvement program is designed to evaluate and promote the internal audit function’s conformance with the Standards, achievement of performance objectives, and pursuit of continuous improvement. This includes internal and external assessments.

The internal assessment should include ongoing monitoring, periodic self-assessment, and communication with the board on the result of the assessment. The board and chief audit executive should determine the frequency that is deemed as appropriate to conduct an external assessment as some organization or industries may prefer or be required to increase the frequency or scope of the external quality assessments more frequently than every five years.

KEY STEPS IN IMPLEMENTING THE NEW STANDARDS

Here are key steps for considerations when preparing the implementation:

- Assess Readiness

- Understand the 2024 Standards (there are many resources to guide in the IIA’s website).

- Evaluate your current policies and practices against the 2024 Standards.

- Identify gaps and areas for improvement.

- Prioritize necessary changes based on their impact and urgency.

- Understand the 2024 Standards (there are many resources to guide in the IIA’s website).

- Create a Plan

- Develop a roadmap for implementing the required changes.

- Align your internal audit strategy with the new Standards.

- Consider how internal audit can contribute to achieving the organization’s vision and resilience.

- Develop a roadmap for implementing the required changes.

- Implement the Plan

- Execute the prioritized changes outlined in transformation plan.

- Communicate the new requirements to board of commissioners, board of directors, audit committees, and senior management.

- Execute the prioritized changes outlined in transformation plan.

Remember, the new Standards impact the entire organization, so collaboration and alignment across teams are essential, and do not shy away from engaging with stakeholders as it will helps in ensuring a smooth transition.