RSM INDONESIA CLIENT ALERT – 20 March 2025

In recognition of difficulties faced by taxpayers to pay and/or report taxes using the Coretax tax administration system, on 27 February 2025, the Director of General Taxation (DGT) issued Decision No. KEP-67/PJ/2025 concerning the Policy regarding the Elimination of Administrative Penalties on Late Payment and/or Deposit of Tax Due and the Late Submission of Tax Returns related to the implementation of Coretax (KEP-67).

WHEN IS IT EFFECTIVE?

KEP-67 is effective on 27 February 2025 (although it has retroactive effect for tax penalties that would otherwise be due for late payment and/or late reporting of taxes for certain tax periods).

WHAT DOES KEP-67 PROVIDE?

KEP-67 provides the basis for DGT officials to not issue tax collection letters (surat tagihan pajak) that would otherwise be issued due to the late payment/deposit of taxes and/or late reporting of tax returns for certain periods. Further, if a tax collection letter has already been issued for late payment and/or reporting of taxes for that period, then the Head of the Regional Tax Office is authorized to cancel the tax collection letter.

This is implemented through provision of extended time deadlines for payment/deposit and/or reporting of certain taxes.

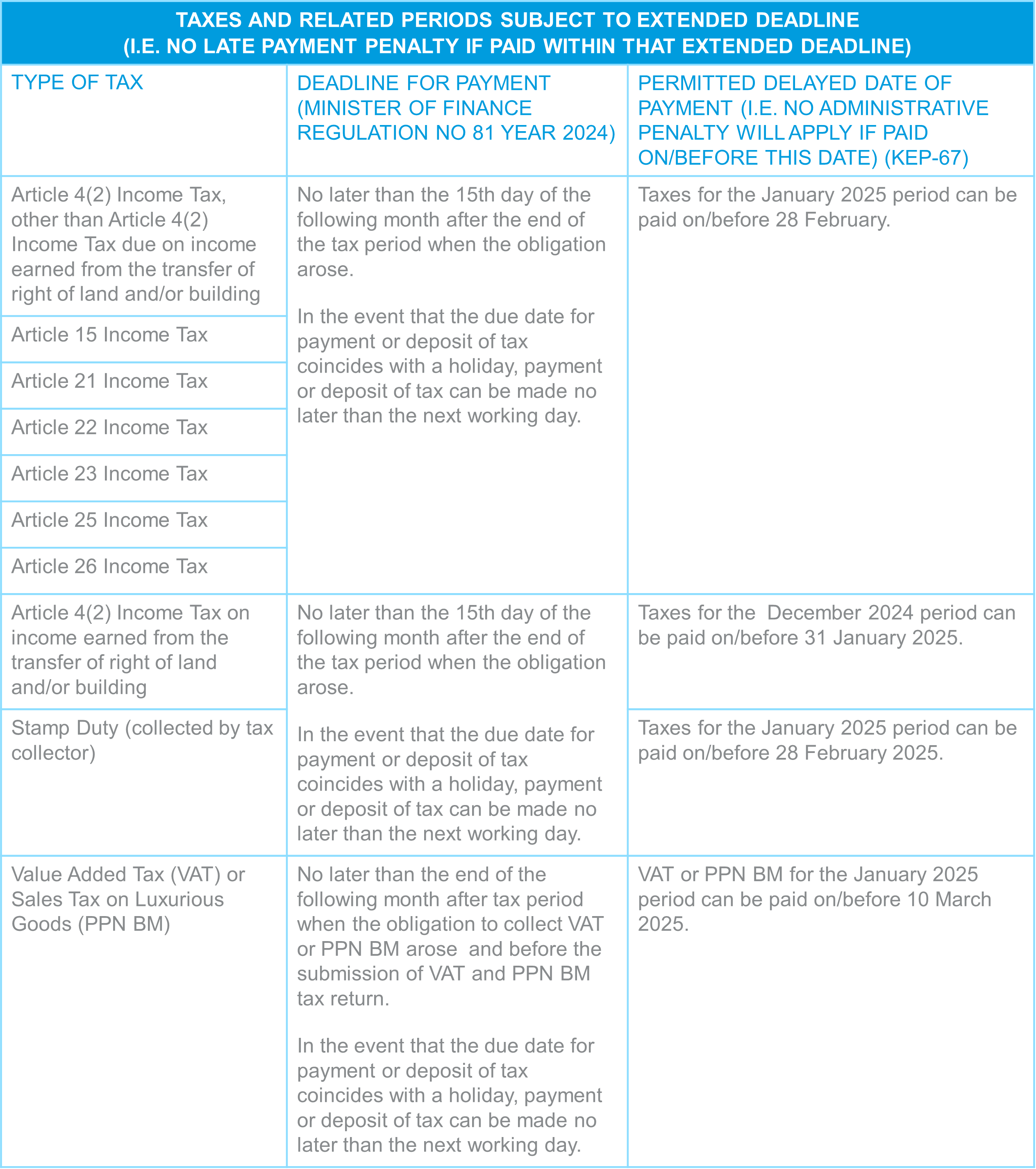

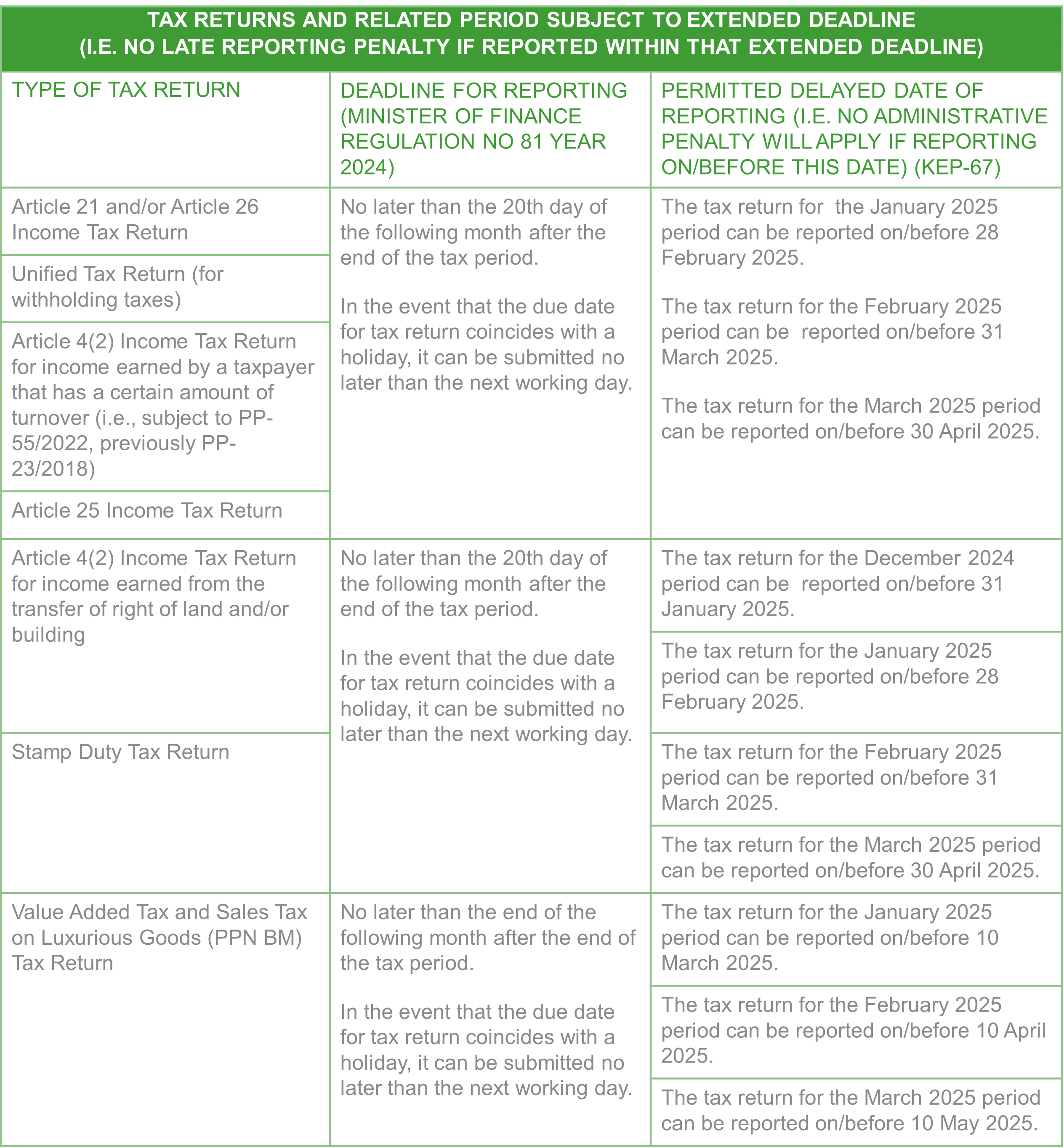

WHAT LATE PAID TAX PAYMENTS/DEPOSITS AND LATE REPORTED TAX RETURNS ARE SUBJECT TO KEP-67?

The table below details the types of taxes and periods that are subject to KEP-67.

RSM COMMENTS

- The relaxation of administrative penalties for late payment of taxes is strictly limited to the tax periods of December 2024 (for limited taxes) and January 2025. It is possible KEP-67 might be amended and/or an additional decision letter will be issued regarding the waiver of late payment penalties for the tax periods of February 2025 and March 2025.

- The penalty waivers only apply if the tax is paid/deposited and/or reported within the extended deadline. If this is missed, then the usual penalty will apply. In the case of late payment penalties, that penalty will be calculated from the date when the tax should have been paid/deposited as per the general regulations and not the extended deadline.