RSM INDONESIA CLIENT ALERT – 14 January 2025

In accordance with the VAT Law, the VAT rate was required to increase to 12% no later than

1 January 2025. After considering concerns that the imposition of 12% would negatively impact the economy, the Government decided to limit the full impact of the VAT rate increase. Rather than amending the VAT Law that would have taken time (or, possibly, required a Government Regulation in Lieu of Law) this has been achieved through the release of Minister of Finance (MoF) Regulation No 131 Year 2024 dated 31 December 2024 concerning “Treatment of VAT on Imported Taxable Goods, the delivery of Taxable Goods and Services, the utilization of Taxable Intangible Goods and Services from outside the Customs Area into the Customs Area” (PMK-131).

The use of a MoF regulation rather than a revision to the VAT Law also retains future flexibility to amend/revoke PMK-131 and expand the full impact of the 12% rate across those goods and services that PMK-131 regulates as only being subject to an effective VAT rate of 11%.

WHEN DOES PMK-131 APPLY?

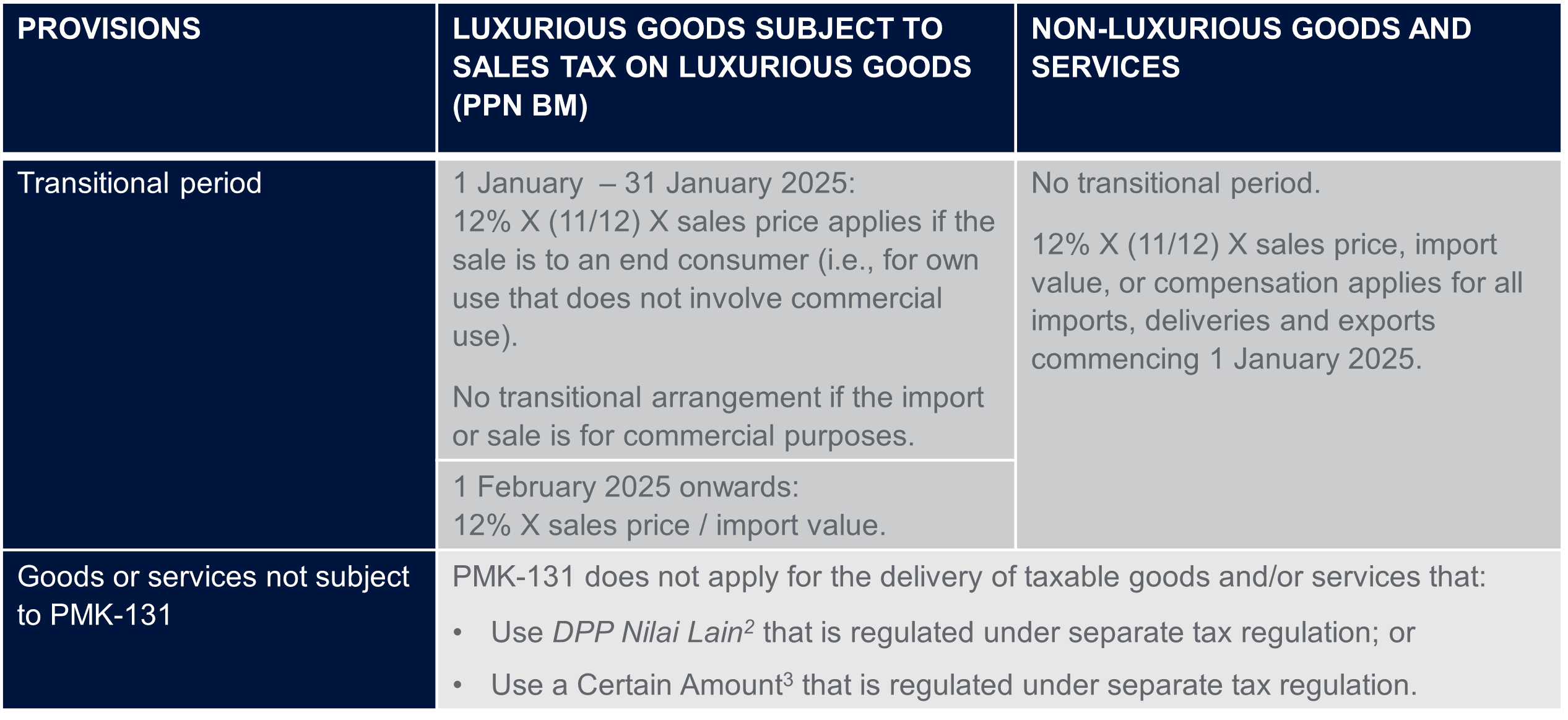

PMK-131 is applicable starting 1 January 2025 to reduce the effect on most taxable goods and services of the increased VAT rate.

HOW DOES PMK-131 ADJUST THE IMPLEMENTATION OF THE 12% RATE?

In general, PMK-131 provides that most taxable goods and services will use an Other Tax Base (DPP Nilai Lain) equal to 11/12 of the import price, selling price or compensation, so that the effective VAT rate remains 11% (i.e., 11/12 x 12% = 11%).

The exceptions are luxurious goods, goods or services that are already subject to DPP Nilai Lain, or those subject to VAT using a Certain Amount (a specified rate other than the general VAT rate).

The table below summarizes the key aspects of the regulation:

1Luxurious goods are defined under MoF Regulation No 141/PMK.010/2021 concerning the Stipulation of types of Motorized Vehicles subject to Sales Tax on Luxurious Goods and Procedure for the Imposition, Granting, and Administration of Exemption, and Refund of Sales Tax on Luxurious Goods, and Regulation No 15/PMK.03/2023 concerning the amendment of Regulation No 96/PMK.03/2021 concerning the Stipulation of types of Taxable Goods other than Motorized Vehicle subject to Sales Tax on Luxurious Goods and Procedure for the Exemption from Imposition of Sales Tax on Luxurious Goods.

Luxurious goods in form of motorized vehicles are: (a) motorized vehicles for transporting up to 15 people; (b) motorized vehicles with double cabins; (c) golf cars (including golf buggies) and similar vehicles; (d) special vehicles for snow, on the beach, in the mountains, or technical vehicles; (e) motorized vehicles with 2 or 3 wheels with piston engines with a cylinder capacity exceeding 250cc; (f) trailers, semi-trailers of the caravan type, for housing or camping; (g) motorized vehicles with a cylinder capacity exceeding 4,000cc.

Luxurious goods other than motorized vehicles are: (a) firearms and bullets other than for state purposes; (b) aircraft with propulsion, other than for state purposes or commercial air transport; (c) air balloons (d) cruise ships, excursion ships, and/or similar vessels other than for the state or public transport; (e) yachts, other than for the state, public transport or tourism businesses, and (f) residences (house, apartment, etc) with a selling price of Rp 30 billion or more.

2Goods/services subject to DPP Nilai Lain include: (a) taxable goods and/or taxable services for own use, and (b) free of charge granting of taxable goods and/or taxable services.

Since PMK-131 does not apply therefore the 12% VAT rate will apply. For example, if the transaction involved the consumption of taxable goods for own use, then the VAT will be determined as 12% x (purchase price - margin) compared to the calculation prior to 1 January 2025 that would have used 11% x (purchase price - margin).

3Goods/services subject to Certain Amount include: (a) self-building activities (Kegiatan Membangun Sendiri); (b) the delivery of certain agricultural products and used motor vehicles, (e) the delivery of certain services such as: package delivery services; travel agency/ tourism agency services; freight forwarding services; marketing services with vouchers; crypto asset trading; and Insurance agency services.

Since PMK-131 does not apply therefore the 12% VAT rate will apply. For example, if the transaction was for freight forwarding services, then the VAT will be determined as 1.2% (i.e., 10% x 12%) X transaction amount compared to the calculation prior to 1 January 2025 that would have used 1.1% (10% x 11%) X transaction amount.

RSM COMMENTS

- If the sale/delivery of taxable goods or services previously used “01” for the VAT invoice code then the code will become “04” commencing 1 January 2025.

- Since the effective continuation of the old 11% rate for most taxable goods/services is regulated through MoF regulation, therefore it can be changed any time the Government decides the economy is “ready” for the full imposition of the 12% rate across a wider range of taxable goods and services.

- Accounting systems (and commercial invoice templates) should be revised to correctly identify the applicable VAT rate and actual VAT.

- In recognition of the challenges that some business might face, the Director-General of Taxation, through regulation PER 1/PJ/2025, has stated the VAT invoice (and other documents that are treated similar to a VAT invoice) during the period from 1 January - 31 March 2025 will still be considered to comply with the tax regulations even though:

- The Tax Base uses the full transaction value/ replacement price/ import value and the 12% VAT rate (instead of DPP Nilai Lain), or

- The Tax Base uses the full transaction value/ replacement price/ import value and the 11% VAT rate.

- The Tax Base uses the full transaction value/ replacement price/ import value and the 12% VAT rate (instead of DPP Nilai Lain), or