The ESG compliance landscape has been rapidly evolving, and there has been no more proof of this than the recently communicated Omnibus Simplification Package, which has introduced significant revisions to existing ESG regulations and the Corporate Sustainability Reporting Directive (“CSRD”) in particular.

This article is written by Gidion Lont (GLont @rsmnl.nl), Iman Zalinyan ([email protected]) and Mario van den Broek ([email protected]) . Gidion, Iman, and Mario are part of RSM Netherlands Business Consulting Services, specifically focusing on Sustainability and Strategy.

1. Setting the context

Omnibus has been presented to reduce the regulatory burden on companies, adjusting CSRD, CSDDD, CBAM, and the EU Taxonomy. The most impactful proposed adjustments for CSRD are the reduction of the scope of companies affected by 80%, and a reduction in data points to be reported. It is important to note that various other ESG regulations are expected to proceed as planned. The European Council has recently adopted a position on the proposed "stop-the-clock" mechanism related to the Omnibus. On April 1st, the EU Parliament approved the urgent procedure for the proposal, and the vote on April 3rd made the implementation delay definitive whereby it was decided on a two-year delay in the application of the CSRD for companies that have not yet begun reporting, and a one-year postponement of the transposition deadline for the CSDDD.

2. The role of SME’s and family owned businesses in a sustainable future

Although SMEs and family-owned businesses were not impacted by the CSRD and Omnibus proposals immediately, there is great value in adopting ESG strategies and reporting structure. Since many SMEs and family-owned businesses are clients or suppliers to large corporations, their supply chain partners have started to expect a certain level of ESG adoption. We have observed that many SMEs face extensive information requests from their business partners, which they either cannot answer sufficiently or only act on an ad hoc-basis. Although information gathering seems to be the main demand for SMEs from large supply chain partners, SMEs are expected to provide ESG performance and compliance with supplier codes of conduct as the next steps. By introducing ESG reporting strategies that are proportionate to their size, SMEs can streamline their efforts to fulfill the needs of their business partners and ensure that they remain long-term business partners.

SME’s are often described as the backbone of the economy, accounting for more than 60% of all businesses in the EU and 1 in 7 Dutch businesses, including 18% of large companies (over 250 FTE). According to CBS (2022), SMEs employ 31% of the full Dutch workforce. Given their family heritage, SMEs tend to have strong values, often based on the family's culture, traditions, and ethical principles. While working with family businesses extensively, RSM found that many families have been integrating ESG for a long time because it is part of their nature. Therefore, their approach to ESG integration often is not explicitly intended or structured, and many SMEs are even unaware of their ESG perspectives because it is part of ‘just the way we do business around here’. Through this natural and unplanned approach, SMEs risk losing out on the opportunity to exploit this untapped potential of ESG integration organizationally and commercially. In addition, uncertain EU regulatory requirements caused by the Omnibus Package, changing consumer demands, and increasing investor expectations make structured and strategic ESG adoption a necessity rather than an option. This article explores the unique opportunities and challenges of ESG integration in family-owned businesses in the uncertain post-omnibus ESG landscape.

SMEs generally have a very specific set of business characteristics compared to other businesses. Because of the personal involvement of the family, their values often shape their approach to customers and employees, and responsible business standards, emphasizing trust, loyalty, and long-term relationships. Since they have been operating in the same area for generations, they have deep connections with local communities, leading to stronger stakeholder focus and engagement than other businesses.

For example, they seek long-term relationships with customers and suppliers, prioritizing fair business practices and creating a reputation for reliability and consistency. This is also exemplified by having more personal relationships with their employees as they tend to see them as an extension of their own families, resulting in increased loyalty and lower employee turnover rates. As family-owned businesses are passed down from generation to generation, they usually take a long-term perspective focusing on creating a legacy and maintaining the business for future generations. These unique characteristics are ideally suited to embrace sustainability principles, causing many SMEs to instinctively integrate ESG principles in their organizations and business relationships.

Although the described characteristics set SMEs up for successful ESG integration, various challenges are remaining. Dealing with the challenges presented by today’s dynamic ESG landscape, uncertain regulatory environment and changing stakeholder expectations requires structured and strategic approach to dealing with ESG. As ESG regulations are being implemented, SMEs must formalize their ESG integration to comply with supply chain and transparency obligations. At the same time, the recent Omnibus proposals cause a high level of uncertainty about the legal landscape, requiring a new strategic and flexible approach to ESG. However, SMEs often lack concrete ESG strategies and formalized internal (reporting) infrastructures to manage these complexities.

Furthermore, integrating ESG offers companies many benefits, including efficiencies and better stakeholder relationships. In addition, many stakeholders including clients and investors increasingly expect ESG transparency from their supply chain partners to fulfill their objectives and compliance obligations such as CSRD. To unlock these benefits, taking a clear perspective on ESG and being transparent on their ESG performance is required to showcase efforts to demanding stakeholders.

In formalizing ESG integration, SMEs may face some specific challenges. SMEs have a tendency be more conservative in their approach to innovation and risk. This is partly due to a desire to protect the family legacy and avoid jeopardizing the business’s stability. However, some family businesses can also take bold steps if the family values innovation. Since many family businesses prefer self-financing their operations, leading to challenges to do the investments necessary to formalize ESG within the firm. Many SMEs lack formal governance structures, such as independent boards or clear policies, leading to inefficiencies. In addition, they often rely on their capabilities rather than searching for external support. If ESG capabilities in SMEs are unavailable, formalizing ESG strategies and (reporting) structures may present challenges to these companies.

3. Building a sustainable ESG strategy

It is essential to recognize that the landscape of corporate responsibility is evolving, not diminishing. Therefore, we see the Omnibus simplifications as an opportunity for companies to shape their future. CSRD forced companies to adopt a strict framework, set up specific processes and record their steps to obtain an auditor's approval.

Without CSRD compliance and compulsory audit requirements, companies can determine their own ESG journey, free from any external regulatory requirements. They can, therefore, develop an ESG strategy and reporting infrastructure that fits their objectives and ambitions. This way, companies can return to engaging with ESG in a way that makes business sense, takes advantage of emerging opportunities, and decreases business risks. For many companies, stakeholders such as customers, employees, and investors have expectations, and other ESG regulations still apply based on products, processes, or supply chain demands. In addition, opportunities for tapping into new markets, developing sustainable product lines, and saving on costs remain unchanged. Also, larger companies will continue to pursue ESG, collecting data and requiring their partners within the value chain to do the same.

The freedom for a company to design its own ESG strategy comes with great flexibility and opportunity but is also challenging. Companies must carefully consider why they embark on this journey, what drives them and why. Certainly, post-Omnibus, it is essential to either design an ESG strategy, or, when a company has already designed an ESG strategy, it may have to reconsider some of its applied principles, especially in case the CSRD is no longer leading.

Below are some key options that may be adopted.

- Compliance-Driven Approach: Focuses on meeting minimum regulatory and legal requirements (e.g., EU CSRD, SEC Climate Disclosure, SFDR). Best for organizations at the early stages of ESG adoption.

- Value-Creation Approach: Embeds ESG into business strategy to drive long-term value, innovation, and competitive differentiation. Includes sustainable product development, circular economy principles, and impact investments.

- Stakeholder-Centric Approach: Prioritizes engagement with investors, employees, customers, regulators, and communities. Uses frameworks like materiality assessments to identify key ESG priorities.

- Integrated ESG Approach: Embeds ESG across all business functions, aligning with corporate governance, supply chain management, and operational efficiency. Often linked to sustainability-linked financing and performance incentives.

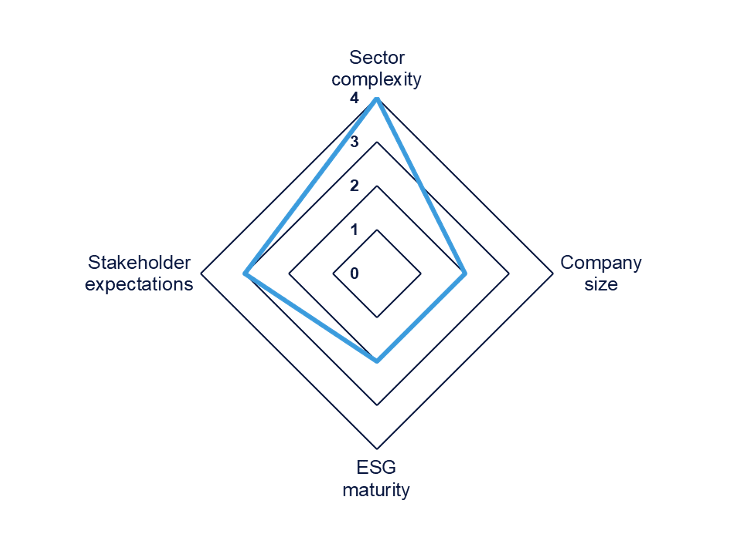

Ultimately, the design or redesign of an ESG strategy must be paired with a decision or at least a consideration of how that strategy results in a specific ESG Reporting Infrastructure. In this respect, a 3-step process may be considered where a company believes its current ESG Maturity, connected to a renewed assessment of its ESG profile to design a (revised) ESG strategy and reporting infrastructure (potentially shifting from CSRD principles to other reporting standards such as GRI, or VSME). Below, we have summarized this as follows:

Maturity

Given the varying factors influencing ESG adoption, companies may consider taking a structured approach to determine whether, how, and to what extent they should integrate ESG into their operations. ESG is not a one-size-fits-all requirement—some companies must comply with strict regulations, while others can leverage ESG strategically for financial or market advantages. Our approach enables companies to consider these differences in their ESG strategy and reporting infrastructure, ensuring it fits their unique circumstances and supports their business objectives.

ESG profile

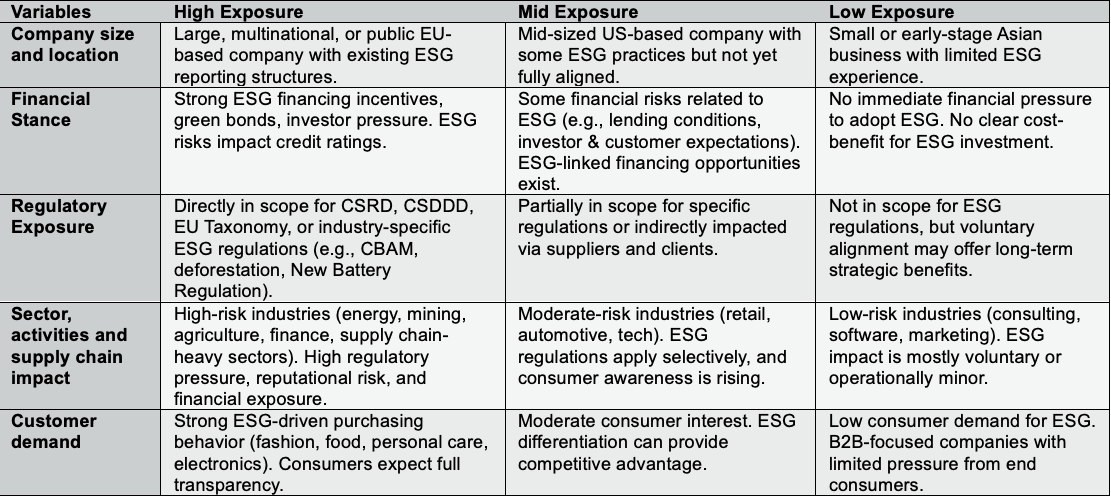

The strategic importance of ESG differs from company to company based on its unique circumstances and its external context, resulting in high complexity for companies in determining the best way to navigate the current uncertainties. This could be due to factors such as stakeholder pressure, investor expectations or regulatory exposure. To determine a suitable ESG strategy, RSM developed an assessment of the ESG profile based on a set of standardized criteria such as company size, financial stance, regulatory exposure, sector, activities, and supply chain, as well as customer demands.

Since these variables are often interconnected, their effect on the importance of ESG integration can increase exponentially if various variables are combined. For example, a large EU-based company that produces highly visible consumer products with complex supply chains faces more stakeholder expectations than a small-scale US-based local service provider.

The decision matrix below contains examples of various high-level outcomes of an ESG profile, which could result in a multitude of company-specific combinations.

For more details and background on the specific variables, please find our whitepaper ‘’CSRD is off the table (for now), but what about ESG?’’ here.

Design of an ESG Reporting Infrastructure

An ESG strategy is designed to help companies manage risks, drive sustainable growth, and create long-term value by integrating ESG principles into their operations and decision-making. It creates clarity and provides direction, which is highly necessary given the current uncertainty in the EU. The need for and the importance of this strategy, as well as its composition, can be determined by the company’s ESG maturity and its ESG profile, as described in the previous sections. When determining an ESG Reporting Infrastructure, organizations have several approaches depending on their maturity level, industry requirements, stakeholder expectations, and regulatory landscape. This may be visualized as follows.

Example

A medium-sized logistics company with 180 employees successfully built its ESG reporting infrastructure by starting small and scaling gradually. They began by focusing solely on tracking their carbon emissions using a simple spreadsheet-based system aligned with the CO2 Performance Ladder methodology. This initial focus required minimal investment but delivered immediate benefits: they identified that idling vehicles accounted for 12% of their fuel consumption, leading to operational changes that saved €32,000 annually. As they progressed to level 3 certification on the CO2 Performance Ladder, they gradually expanded their reporting to include waste management and employee training metrics. As the VSME has been adopted, the company is implementing this as a framework to align with regulatory standards.

A proper ESG Reporting Infrastructure is essentially a selection, prioritization, and organization of the various components described below. Not all components have to be equally extensive depending on your strategy but must be balanced to match the strategy correctly. Depending on the strategy, companies may select an ESG reporting framework. Although reporting without a framework is possible, it is not recommended. Selecting the appropriate reporting framework ensures designing a coherent and organized report, increases consistency and comparability, decreases the risk of greenwashing, and enhances stakeholder trust. Some options are adopting ESRS (for CSRD), Voluntary standards for small- and medium-sized undertakings (VSME, voluntary ESRS-based), Global Reporting Initiative (GRI, voluntary), or ISSB (used mainly by multinational corporations outside of EU).

Building an ESG reporting infrastructure doesn't need to be complex or resource-intensive. The key is creating a system proportionate to your organization's size and aligned with your specific business goals. For very large companies, that means adopting the complete ESRS standards if they are in scope of CSRD. For smaller firms, however, there are many tools that many tools can be used to start their ESG journey, to start progressing, and learn along the way. Adopting the newly developed VSME standards allows SMEs to start reporting based on a complete framework which is aligned with regulatory reporting under CSRD, offering lower complexity and comprehensiveness.

Other frameworks include CO2 Performance Ladder reporting, which is particularly valuable for SMEs in construction, manufacturing, and logistics. It offers a simple way to start reporting on carbon, specifically designed for SMEs. This certification offers a 5-level approach that allows companies to start simply and progress at their own pace. SMEs benefit from specific exemptions at higher levels, making it more accessible than many other frameworks. Companies certified at level 3 or higher often receive preferential treatment in public tenders, creating a direct business incentive.

For ESG reporting purposes, companies must organize data collection internally and throughout their supply chain. Data collection and management ensure ESG reporting is accurate, reliable, and transparent. Companies can assess risks, meet regulatory requirements, and improve sustainability by tracking key metrics like emissions, diversity, and governance practices.

4. Now is the time to reassess, realign, and reimagine.

The path forward for companies navigating this reshaped landscape is clear: Act now, with purpose. The Omnibus Package is not a regulatory pause but an invitation to redefine ESG as a catalyst for growth. Here’s how to seize this opportunity using RSM’s 3-step process:

- Reassess ESG Maturity: Begin with a diagnostic audit of your current capabilities. Identify gaps in governance, risk management, and stakeholder engagement. This assessment is not merely a compliance exercise—it's a chance to uncover hidden opportunities, such as cost savings through circular economy practices or innovation in sustainable product lines.

- Define Your ESG Profile: Align your strategy with your unique context.

- Build a scalable ESG Reporting Infrastructure: Adopt agile tools and frameworks that grow with your ambitions. Implement ESG software to automate data collection, ensure audit-ready controls, and generate insights for decision-making. Transparent reporting mitigates greenwashing risks and improves access to green financing and partnerships.

Although SMEs will face several challenges in setting up ESG infrastructure, their natural integration of ESG perspectives throughout their organization is an excellent feature in unlocking their potential. However, integrating ESG and making the right decisions on ESG reporting requires a structured and objective approach.

The window to lead is open—transform ESG from a mandate into a market advantage. RSM stands ready to guide your journey, offering tailored strategies that turn sustainability into your strongest asset. RSM is a thought leader in the field of Strategy and Sustainability. We offer frequent insights through training and sharing of thought leadership based on a detailed knowledge of industry developments and practical applications in working with our customers. If you want to know more, please contact one of our consultants.