Key takeaways

A ministerial decree dated 25 February 2025 (published in the Official Journal on 27 February, text no. 24) introduces amendments to the rules governing the valuation of vehicle-related benefits in kind. These changes are generally less favourable for employers and employees, increasing the overall cost.

It is important to recall that benefits in kind are considered part of remuneration and must, like regular wages, be included in the basis for calculating social security contributions and charges.

The rules vary depending on whether the vehicle was made available before or after 1 February 2025.

The Official Bulletin of Social Security (BOSS) provided further clarification on these new rules in March 2025.

Our RSM experts provide a comprehensive update on this important topic, which is particularly relevant for companies, especially in the context of URSSAF inspections or employment tribunal disputes.

Discover our infographic at the end of the article

What is a “Benefit in Kind”?

A benefit in kind refers to the provision or availability of goods or services that allow an employee to avoid expenses they would normally incur. It is a form of remuneration that, just like salary, must be included in the base for social security contributions (BOSS – AN – 20).

Such benefits may include use of a vehicle, provision of meals, housing, or tools stemming from new information and communication technologies (“ICT”).

It does not matter whether the benefit is provided by a third party, as long as it is granted due to the employee’s relationship with the company.

The value of such benefits must appear on the employee’s payslip at their gross value.

Important note: :

In addition to the risk of an URSSAF reassessment, it should be reminded that failure to report a benefit in kind on the employee’s payslip and to pay the corresponding social security contributions may constitute concealed employment.

Concealed employment is punishable by up to 3 years' imprisonment and a fine of €45,000 for individuals (€225,000 for legal entities), along with potential additional penalties such as exclusion from public procurement contracts or a ban on receiving public aid for up to five years (non-exhaustive list). French Supreme Court, Social Chamber, 4 December 2024, no. 23-14259, decision concerning a housing benefit in kind.

Benefits in kind may be granted free of charge or in return for a contribution by the employee. However, the employee’s contribution only reduces the taxable amount of the benefit; it does not affect the valuation method (BOSS – AN – 70).

Does the provision of a company vehicle always consitute a Benefit in Kind?

A benefit in kind is deemed to exist when a vehicle is made available to an employee by the company on a permanent basis and used for personal purposes.

The administration considers the provision as permanent when the employee is not required to return the vehicle outside working hours (e.g., during weekends or holidays).

How is the vehicle benefit valued?

The benefit can be assessed, at the employer’s discretion, based either on actual expenses or on a flat-rate method.

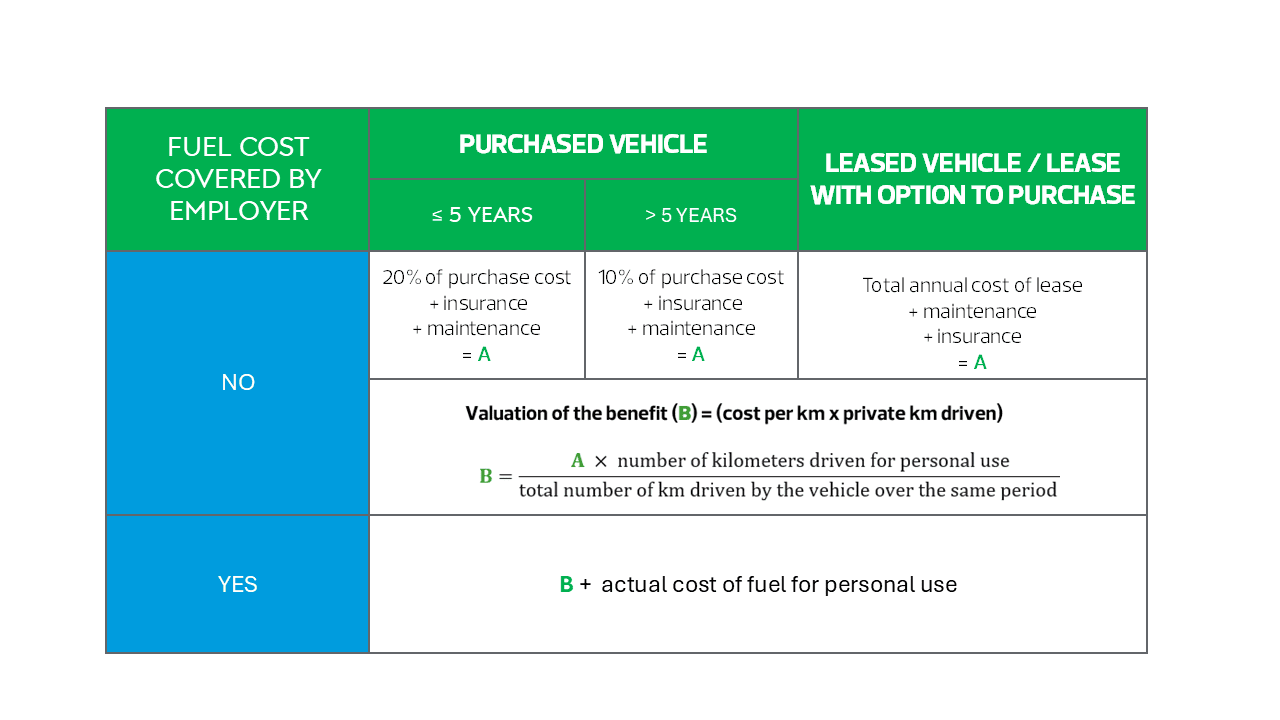

Table n°1: Valuation based on actual costs

According to the BOSS (BOSS – AN – 700), mileage logs, appointments or visit records serve as valid evidence of professional mileage. Purchase cost refers to the total amount including VAT paid by the company.

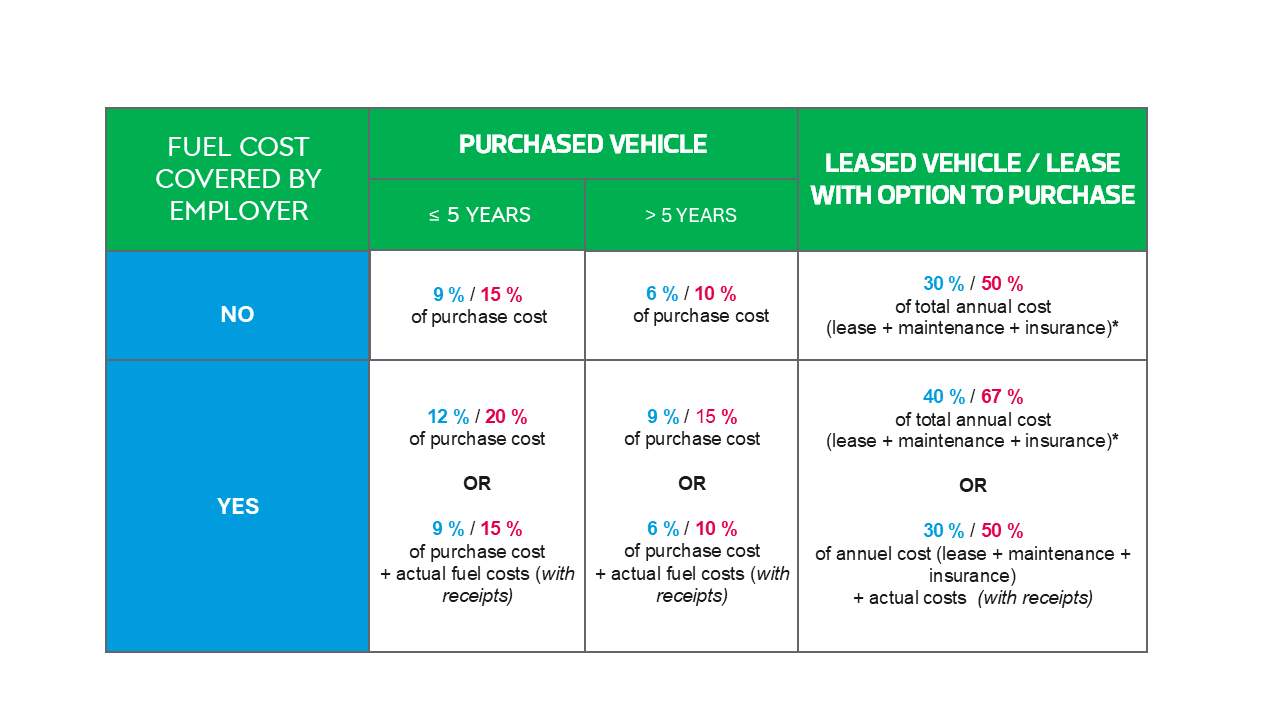

Table n°2: Valuation based on flat-rate method

In blue: Valuation rules for vehicles made available until 31 January 2025

In red: Valuation rules for vehicles made available from 1 February 2025

*: The benefit is capped at the value of the benefit if the vehicle were purchased. The reference price is the gross purchase price (VAT included) paid by the lessor, factoring in any applicable discount, capped at 30% below the manufacturer’s recommended retail price as of the start date of the lease (BOSS – AN – 860, 890).

According to BOSS, the vehicle is considered provided as of the date agreed upon between the employer and employee.

What about fully electric vehicles ?

For vehicles running exclusively on electricity and made available to employees up to 31 January 2025, transitional provisions remain in effect.

BOSS confirms that, whether based on actual cost or flat rate, the valuation excludes electricity costs paid by the employer for charging and benefits from a 50% deduction capped at €2,000.30 annually (rate as of 1 January 2025).

For electric vehicles made available from 1 February 2025:

• Valuation based on actual cost still benefits from a 50% deduction, capped at €2,000.30 per year;

• Valuation based on flat-rate benefits from a 70% deduction, capped at €4,582 per year.

In addition, to qualify for these deductions, electric vehicles made available from 1 February 2025 must meet a minimum eco-score requirement, verified on the date they are provided to the employee.

When an employer and employee agree on the assignment of a company vehicle, it is strongly recommended to define the respective obligations in the employment contract.

This may involve matters such as:

• Costs related to restoring the vehicle to its original condition or paying fines for traffic offences committed by the employee;

• Personal use of the company's fuel card;

• The status of the vehicle in the event of employment suspension (e.g., long-term illness).

• etc.

For company vehicles intended for strictly professional use, it is also advisable to formalise the provision, not only to remind the employee of usage rules but also to justify the arrangement to URSSAF if audited.

Depending on the situation, it may be wise to establish a company vehicle policy (including for executive cars) and, where appropriate, incorporate it into the company’s internal regulations.

For tailored solutions that meet the challenges and specifics of your company,

our RSM experts are here to assist you.

Our team of HR consulting and support experts is here to listen to your needs, understand your strategy, challenges, and economic environment. We offer a multidisciplinary, agile, and tailored solution.

Discover our HR, Social, and Payroll Consulting Services.