Key takeaways

According to Dares, more than 500,000 people used the mutual agreement termination in 2022. Fifteen years after its creation, it is clear that it has become the third most common way to end a permanent contract (CDI), after resignations and dismissals. As a consequence of the pension reform, the procedures for Individual Mutual Agreement Termination (RCI) will evolve starting September 1, 2023. What are the changes that will take place from September 1, 2023?

The Origin, Procedures, and Objectives of the Reform of Mutual Agreement Termination

Origin and Procedures of the Mutual Agreement Termination

In the early 2000s, debates began on the need for a third way of ending permanent contracts (CDIs), combining the advantages of both dismissal and resignation, without their respective drawbacks.

Successive reports (Virville in January 2004, labor market modernization negotiations in 2007, and Attali in January 2008) mentioned terms such as "negotiated termination," "separation or mutual agreement termination," and "amicable termination."

The Mutual Agreement Termination was formally introduced following the National Interprofessional Agreement (ANI) on January 11, 2008. It was later incorporated into the French Labor Code through the law of June 25, 2008, "Modernizing the Labor Market." The law outlines four specific aspects for this type of contract termination:

- No indication on the initiative or reasons for the termination,

- Termination compensation is at least equal to the legal dismissal compensation (or higher if stipulated in the collective agreement),

- Approval through administrative homologation to prevent disputes. For protected employees, approval by the labor inspector substitutes for homologation,

- Access to unemployment insurance.

Evolution of Mutual Agreement Termination and Pension Reform

During discussions about raising the retirement age, the social security regime for mutual agreement termination was criticized for encouraging employers to terminate older employees. A study by UNEDIC, published in March 2023, highlights a correlation between the legal retirement age and the unemployment rate for seniors. The study shows a significant increase in RCI cases when workers reach the age of 59.

In 2021, according to the UNEDIC study, RCI accounted for 25% of unemployment benefits for individuals over 59, compared to 17% for those aged 56.

As a result, UNEDIC believes that, in the future, this "peak" will shift due to new unemployment insurance rules.

As a reminder, since February 1, 2023, the maximum duration of benefits for those 55 years and older has been reduced to 27 months, from the previous 36 months.

Given that the number of RCIs among employees over 50 has been increasing every year (+3% in 2019, +3.2% in 2020, and +4.1% in 2021, according to Dares), the government believes that the social security regime applied to the mutual agreement termination indemnity (IRC) before the legal retirement age encourages employers to terminate older workers. Indeed, the regime applicable to the IRC only requires a 20% employer contribution, compared to 50% for the retirement termination indemnity regime.

Additionally, the possibility of being covered by unemployment insurance until the legal retirement age also encourages, according to some experts, seniors to use RCI as a form of "disguised early retirement."

The pension reform’s goal is to encourage companies to retain their older employees for longer. The 2023 Amended Social Security Financing Law (LFRSS), which includes pension reform, modifies the social security system for RCI and retirement termination indemnities.

By increasing taxes on RCIs before the legal retirement age, the government aims to reduce their occurrence in the later years of employees' careers. The goal is twofold: to prevent workers from moving onto unemployment benefits before claiming their pensions and to increase the employment rate among seniors.

What Changes for Mutual Agreement Termination Starting September 1?

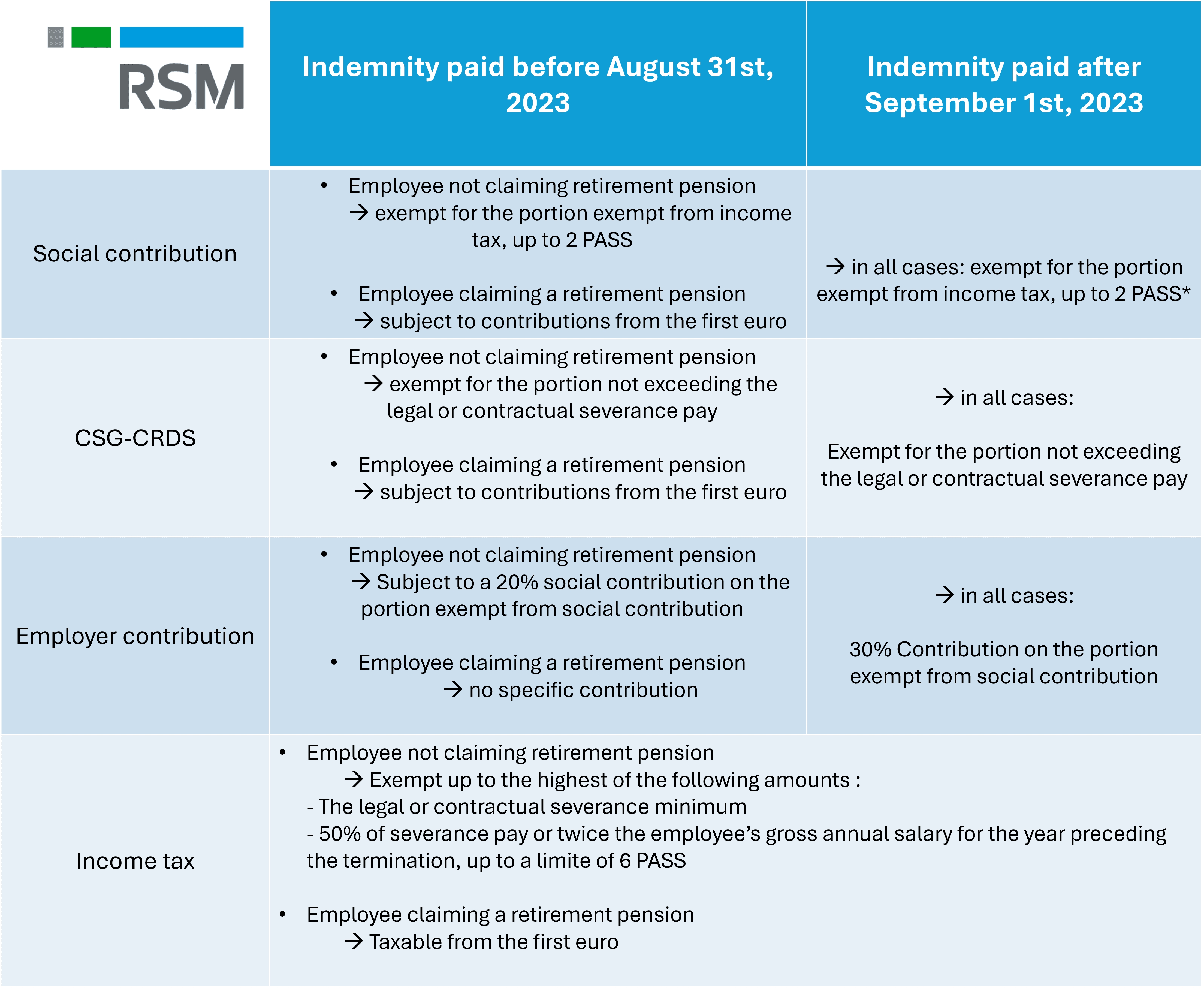

L'indemnité en synthèse

A chart of the social security regime for mutual agreement termination indemnities under the CDI:

PASS: Annual Social Security Ceiling. In 2023, the PASS is set at €43,992.

A Unified Social Security Regime for RCI?

According to the latest updates from the July 2023 Social Flash, the following changes will apply to contract terminations occurring from September 1, 2023:

- The IRC will be exempt from contributions and CSG/CRDS within the limits defined by social security legislation, even when the employee is entitled to a pension from a legally mandatory pension scheme.

- The 20% social contribution will be replaced by a 30% employer contribution on the portion of the indemnity exempt from social security contributions.

No changes are planned on the fiscal side.

Unless modified later by another text, the indemnity will be subject to two regimes:

- Taxable from the first euro for employees entitled to a pension from a legally mandatory pension scheme.

- Exempt within the limits established by tax legislation for other employees.

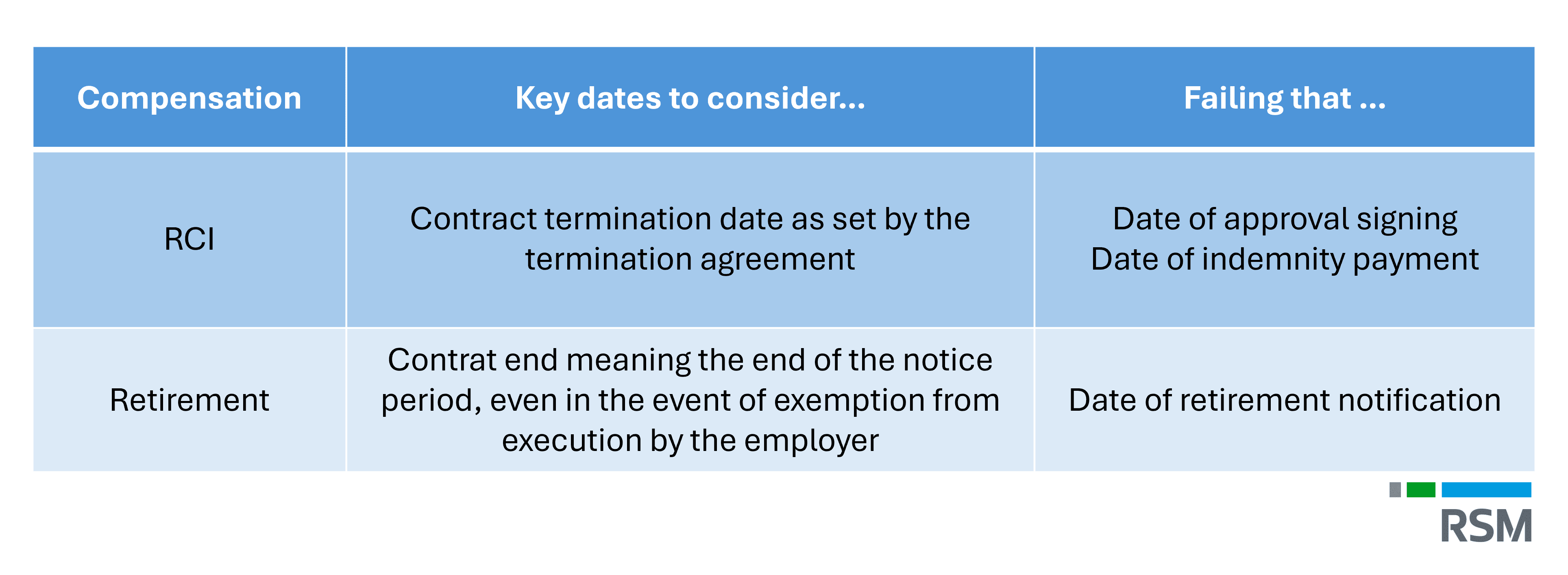

Regarding the effective date of the new social security regime for indemnities, the Official Social Security Bulletin (BOSS) clarified, in an update on August 16, 2023, that the new regime applies to indemnities paid for contract terminations with an effective date after August 31, 2023.

A Less "Costly" Retirement Termination Indemnity

For contract terminations occurring from September 1, 2023, the law eliminates the 50% employer contribution, which was previously applied to the entire indemnity (whether exempt from social security contributions or not).

This will be replaced by a 30% employer contribution, applicable only to the portion of the indemnity that is exempt from social security contributions.

As for other contributions, such as CSG/CRDS and income tax, no changes are planned. The retirement termination indemnity will remain exempt within the same limits as before.

Summary Charts: Copyright RSM France 2023

Corinne Dubost, Manager in employment law

RSM experts support businesses across all sectors in operational management (Payroll, mobility, HRIS...), change management, and interim management.

Discover our HR, Social & Payroll Consulting services.