In recent years, the global tax landscape has witnessed a significant transformation driven by concerted efforts from international bodies such as the OECD, the EU, and the UN. The focus is on combating tax base erosion, creating more tax transparency, and adapting tax systems to modern digital economies. Multinational entities’ (MNEs) tax departments will face in the next decade more tax compliance obligations in the international arena. Tax departments will need to prepare themselves for that to be more in control, not only on a national level but also on a multi-jurisdictional level. New global tax policy initiatives will require that MNEs be able to collect in an automatized manner and verify tax data from group companies in multiple jurisdictions to calculate the correct tax exposure. To become a tax department of the future investing in your global tax governance is paramount in the upcoming decade.

This article is written by Hendrik Bastiaans ([email protected]) and Dick Brinkhof ([email protected]). Hendrik and Dick are both part of RSM Netherlands International Tax Services Practice with a focus on Global Tax Governance.

Understanding Global Tax Governance

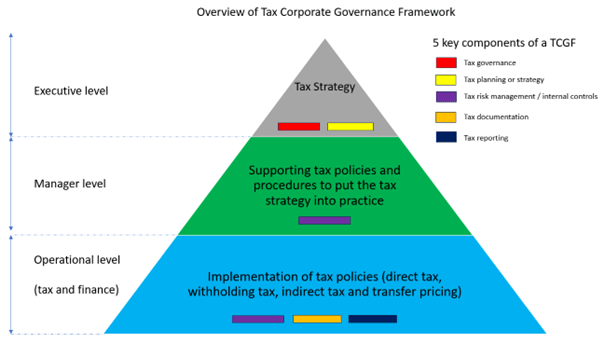

Tax governance includes the formulation of a long-term group tax strategy, clearly formulated roles and responsibilities, tax risk management and control, and an approach to stakeholder engagement. It serves as the compass guiding organizations through the complex web of international tax regulations. It encompasses a set of principles and infrastructure crucial for informed decision-making in global tax issues.

Having a Tax Corporate Governance Framework (TCGF) improves compliance and creates a structured approach for businesses to prepare and adjust to constantly evolving global tax laws and regulations. A TCGF includes fundamental components such as tax strategy, risk analysis, control mechanisms, monitoring, and reporting. Implementing an appropriate framework can effectively manage tax-related risks, reduce long-term costs associated with compliance, and establish a transparent and cooperative relationship between taxpayers and tax authorities.

Furthermore, implementing a robust TCGF holds the potential to significantly diminish future tax compliance expenses. This can manifest through better process efficiencies, better certainty regarding tax positions, enhanced tax risk management, and decreased manpower allocation to compliance tasks. Consequently, the time currently allocated to compliance tasks could be redirected towards more value-generating activities.

Forward-thinking

TCGF will be essential to properly manage the global tax risks of multinational tax departments as they need to provide insights on taxable profits, effective tax rates, and other essential elements that influence their tax position. In that respect, the following tax challenges may be relevant:

- Pillar II is expected to be a major source of potential risk. This is likely due to the laws enacted by jurisdictions to make a Qualified Domestic Minimum Top-Up Tax (QDMTT) and an Income Inclusion Rule (IIR) effective as of 1 January 2024, their interaction with countless other areas of a jurisdiction’s tax regime will need to be thoughtfully considered from a global level. For reporting years starting as of 1 January 2025, an Undertaxed Payments Rule (UTPR) will require increased interaction between tax jurisdictions. The UTPR would apply where the jurisdiction in which a group is headquartered has an effective tax rate below the minimum tax rate. This is because the IIR itself does not apply to the headquarters’ jurisdiction. Any top-up tax then would be collected under the UTPR by the countries in which other group companies are located.

- EU Public Country-by-Country Reporting (EU Public CbCR) is another source of potential risk. Starting from June 22, 2024, the European Union will require new external reporting requirements affecting numerous MNEs. The EU Public CbCR mandates MNEs to prepare and disclose a new dataset to the general public. While primarily aimed at EU branches and subsidiaries, the scope of EU Public CbCR also encompasses many non-EU MNEs, imposing extra disclosure obligations on them. The ability of stakeholders across the world to have an informed opinion as to whether a business is paying the right amount of tax, in the right place, and at the right time, could result in tax reputation risks.

- Looking forward to the future more EU law initiatives are on the legislative train. These require a proper TCGF in place to manage them properly. We see the Business in Europe: Framework for Income Taxation (BEFIT) on the horizon for 2026 (TP proposal) and 2028 (EU Group Consolidation proposal). The new proposal sets out a new framework of tax rules to help all companies in a group to determine their tax base. A one-stop shop will allow the group to file an information return with the tax bases of all the group members with the tax administration of one Member State. Those tax bases will then be aggregated at the EU group level and allocated to each company in the group.

RSM is a thought leader in the field of International Tax and Global Tax Governance. We offer frequent insights through training and sharing of thought leadership that is based on a detailed knowledge of EU Tax Directives, OECD Transfer Pricing Guidelines, OECD Guidance on BEPS initiatives (such as Pillar I and II), and practical applications in working with our customers. If you want to know more, please contact one of our consultants.