With the Corporate Sustainability Reporting Directive (CSRD) taking full effect, organizations are scrambling to meet its comprehensive disclosure requirements. One crucial aspect often overshadowed in these efforts is the obligation to report on the EU Taxonomy. This requirement is not just a box to tick; it is an important factor in determining whether companies can secure limited assurance on their CSRD report—and thus carries significant implications for audit readiness.

This article is written by Bart Ladru ([email protected]) & Sefa Geçikli ([email protected]). Bart and Sefa are part of RSM Netherlands Business Consulting Services with a specific focus on Sustainability and Strategy.

Understanding the Obligation

The CSRD requires in-scope companies to disclose information about how their business activities align with the EU Taxonomy. This means that companies must evaluate and report on their activities according to the criteria set out in the Taxonomy Regulation. Therefore, taxonomy disclosures are mandatory and integral part of CSRD compliance. This ensures that companies not only disclose their impact but also report on how their business aligns with the EU's sustainability goals.

While entities under the scope of NFDR have already been reporting according to EU Taxonomy, now large undertakings must comply with Article 8 of the EU Taxonomy Regulation, which outlines transparency obligations for non-financial undertakings. This includes disclosing how their activities align with the Taxonomy’s definition of environmentally sustainable activities.

What Is the EU Taxonomy?

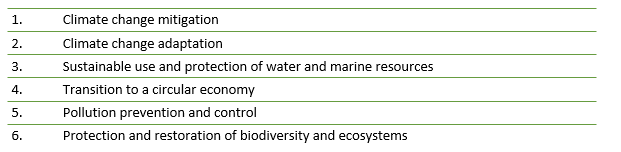

At its core, the EU Taxonomy is a classification system designed to help organizations determine whether their economic activities are environmentally sustainable. To qualify, activities must meet specific criteria as defined in Article 3 of the regulation. This requires a substantial contribution to one or more of the six environmental objectives outlined in Article 9 of the EU Taxonomy Regulation:

For companies, the challenge lies in identifying which of their activities are eligible—meaning they have the potential to make a substantial contribution in a given area—and demonstrating their alignment with these objectives. They need to demonstrate how their products and services contribute to one or more of the key sustainability criteria, while ensuring that their operations do not cause significant harm to other environmental objectives. Additionally, they must comply with minimum safeguards, such as human rights and anti-corruption standards, and meet the technical screening criteria. This reporting structure is crucial for enabling stakeholders—including investors and regulators—to accurately assess the sustainability of a company’s operations.

The Importance of EU Taxonomy in CSRD Audit Requirements

From an audit perspective, EU Taxonomy reporting is critical to achieving limited assurance on CSRD reports. Article 34(1) of the CSRD requires auditors to express an opinion based on a limited assurance engagement, which includes verifying compliance with the directive. A crucial aspect of this is whether the company has met EU Taxonomy reporting requirements, as outlined in Article 8.

The transparency requirements demand that companies provide detailed information on how their economic activities contribute to the six environmental objectives. Additionally, companies must disclose the percentage of turnover, capital expenditure, and operating expenses tied to these sustainable activities. For auditors, the thoroughness of these disclosures is key when assessing whether a company’s sustainability report meets CSRD standards. Failure to adequately report on these activities could result in incomplete or inaccurate audit opinions, jeopardizing compliance.

Forward Thinking

While many organizations concentrate on fulfilling CSRD reporting obligations, the incorporation of EU Taxonomy requirements into CSRD compliance often slips under the radar. Yet, failing to meet these requirements can have significant ramifications. The obligation to report under the EU Taxonomy is not just an exercise in transparency; it is a decisive factor for audit assurance, and by extension, overall CSRD compliance.

Looking forward, companies that embrace the EU Taxonomy not only as a reporting obligation but also as a strategic tool will be better positioned to thrive in an increasingly regulated environment. Integrating Taxonomy into core business practices can help firms identify areas for operational improvement, drive innovation in sustainable products and services, and attract green investments.

Moreover, companies aligned with the EU Taxonomy are more attractive to investors. This alignment can enhance access to green loans, sustainable bonds, and investment from institutions prioritizing environmentally sustainable portfolios, lowering the cost of capital. Taxonomy alignment signals a company's commitment to sustainability.

In conclusion, the EU Taxonomy’s role in the CSRD is far more than an administrative requirement. It is an essential component for securing limited assurance on sustainability reports and should be treated as a top priority for companies aiming to maintain compliance and enhance their sustainability performance. Forward-thinking companies will not only meet these obligations but will leverage them to drive innovation, resilience, and long-term success in the face of global sustainability challenges.

RSM is a thought leader in the field of Sustainability and Strategy consulting. We offer frequent insights through training and sharing of thought leadership based on a detailed knowledge of industry developments and practical applications in working with our customers. If you want to know more, please contact one of our consultants.