Approximately 20% of the Dutch population and 27% of individuals over the age of 16 within the European Union experience various levels of disabilities. Addressing this, the European Accessibility Act (EAA) aims to standardize accessibility regulations across EU Member States. This legislative move not only safeguards the rights of individuals with disabilities but also enhances cross-border trade and broadens market access for businesses. By mandating the redesign of products and websites to be accessible to everyone, the EAA introduces both compliance requirements and business opportunities. Products and services adhering to the EAA's standards will enjoy the privilege of free movement across the EU, exempt from additional national regulations. This facilitates greater market penetration for companies and opens a new customer base, including people with disabilities and the elderly. Many banking services fall under the scope of the EAA. Redesigning products and services for accessibility is not an overnight task, the time to start preparing for compliance is as the deadline is approaching. This article provides a brief overview of the banking services covered by the Act and outlines key steps financial institutions should take to ensure compliance.

Banking services covered by the EAA

UThe European Accessibility Act (EAA) targets key products and services that are vital for individuals with disabilities and that historically have had inconsistent accessibility standards across EU nations. It mandates full accessibility for these offerings. The Act applies uniformly to all products and services in the scope available within the EU market, irrespective of whether they are produced within the EU or imported. Consequently, any private sector entity distributing products or services in the EU must adhere to the provisions of the EAA.

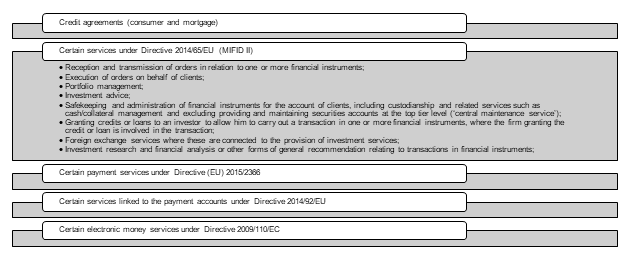

Regarding banking and financial services, Union law on banking and financial services aims to protect and provide information to consumers of those services across the Union but does not include accessibility requirements. With a view to enabling persons with disabilities to use those services throughout the Union, including where provided through websites and mobile device-based services including mobile applications, to make well-informed decisions, and to feel confident that they are adequately protected on an equal basis with other consumers, as well as ensure a level playing field for service providers, this Directive establishes common accessibility requirements for certain banking and financial services provided to consumers. The EAA applies to the following services provided to consumers -any natural person who purchases the relevant product or is a recipient of the relevant service for purposes which are outside his trade, business, craft or profession-:

The appropriate accessibility requirements also apply to identification methods, electronic signature and payment services, since they are necessary for concluding consumer banking transactions.

The EAA was adopted by the European Union in June 2019. For the next step, in June 2022, all member states must have translated the EAA and added it into their own national legislation. From 28 June 2025, the European Accessibility Act will come into force. For services placed on the market and contracts entered into before 28 June 2025 there will be an additional transition period of five years. Therefore, service providers may continue using products (e.g., equipment, systems) already in lawful use before 28 June 2030 to provide their services, even if these products do not comply with the Directive's accessibility requirements. Contracts in-scope signed before 28 June 2025 can remain in effect without modification, but only until they expire or for a maximum of five years from that date (i.e., until 28 June 2030). While, Self-service terminals (e.g., ATMs, ticket machines) lawfully in use before 28 June 2025 may continue to be used until the end of their economically useful life, capped at a maximum of 20 years from the date they were first used. On the other hand, even if the service provider chooses to replace any of the existing products (e.g., equipment or self-service terminals) during the transitional period, the replacement must comply with the accessibility requirements of the Directive, even if the original product was placed on the market before the Directive's application date.

Strategies for Financial Institutions

The EAA mandates that products and services:

- Be designed and produced to optimize usability for people with disabilities.

- Adhere to comprehensive regulations regarding information and instructions, user interface and functionality design, support services, and packaging.

The text of the EAA offers insights into what business owners can anticipate. Notably, the Directive specifically mentions the four principles of web accessibility, known as "POUR," affirming their relevance to this Directive. These principles dictate that service offerings must be:

In line with the phased approach of the EAA, financial service providers can prioritize the obligations due in June 2025 and those related to their most impactful and wide-reaching services. They can follow a step-by-step approach:

- Analyze business activities and identify which services are under the scope of the EAA

- Identify compliance requirements for the covered services

- Assess the gap between the current design and the requirements of the Act

- Implement and design for compliance

Forward Thinking

Compliance with the EAA streamlines banking services across the European Union, opening doors to new markets and opportunities while positioning your business as a leader in accessibility. It also expands your customer base by reaching underserved groups, such as the elderly and people with disabilities. In this regard, the EAA is about more than just avoiding penalties.

On the other, member states oversee enforcing their own penalties for non-compliance, which should be “effective, proportionate, and dissuasive.” Each member state must make it possible for consumers to report noncompliance to either the courts or the body in charge of enforcing the law in that country. Both public and private organizations also must have the option of going to court or filing a complaint with the body in charge. In the Netherlands, the Dutch Consumer Protection (Enforcement) Act governs enforcement actions, granting supervisory authorities the power to levy administrative fines or enforce orders with penalties.

Many banking services fall within the scope of the EAA. Redesigning products and services for accessibility is a complex process that takes time, so the best time to start preparing for compliance is now, with the deadline fast approaching.

RSM is a thought leader in the field of Strategy and International Trade consulting. We offer frequent insights through training and sharing of thought leadership based on a detailed knowledge of industry developments and practical applications in working with our customers. If you want to know more, please contact our partner, Mario van den Broek via [email protected].