Starting from January 1, 2025, the Canton of Vaud has made significant changes to the directive on the valuation of unlisted securities for wealth tax purposes for business owners, with the aim of reducing the tax base for company’s shareholder(s). This directive, which has been in force since January 1, 2022, provides important clarifications for valuing unlisted securities.

In the Canton of Vaud, the tax valuation of unlisted securities has long been a concern for entrepreneurs. Unlike the listed shares, whose value is determined by the financial markets, the unlisted securities or shares in companies that are not traded on the stock exchange require more complex valuation methods, which have a direct impact on entrepreneur’s taxable wealth. Furthermore, this valuation is often much higher than the real value of the company, leading to a heavy tax burden for the individual shareholder.

Introduction

Aware of this problem, the State Council of Vaud adopted a decree on the Regulation on the Valuation of Unlisted Securities and Non-regularly Listed Securities for Wealth Tax Purposes on December 8, 2021, simplified under the name of “RETIF". The aim of this directive is to establish a fairer valuation method that better reflects the economic reality of the companies and attempts to reduce the tax base for entrepreneurs in the canton of Vaud. To clarify its application, on November 8, 2022, the Finance Department of the canton of Vaud published a directive based on two key principles.

Firstly, a framework for the valuation of unlisted securities, based on the "Instructions for the Valuation of Unlisted Securities for Wealth Tax Purposes" (hereafter: "Circular 28") issued by the Swiss Tax Conference (CSI), using the practitioners’ method.

Secondly, measures have been introduced for the valuation of unlisted securities in favor of the entrepreneurs operating their own companies, according to certain criteria, thus reducing their tax burden.

The practitioners’ method

The Circular 28 prescribes that the commercial compagnies are valued using a standard valuation method, known as the “practitioners' method”. This method is based on a weighted average of the following two elements: the earnings value (double weighted) and the substance value (single weighted). To determine the substance value, the company’s equity is considered, including any hidden reserves. The earnings value, on the other hand, measures the company's ability to generate profits. It is calculated by averaging the net results of the 2 or 3 last financial years, average which is then capitalized. As an indication, for the 2024 tax year, the Federal Tax Administration has applied a capitalization rate of 8.75% for the valuation of unlisted securities.

Thus, the practitioners' method can be expressed mathematically as follows:

Practice in the Canton of Vaud

The Canton of Vaud has introduced opportunities aimed at reducing the wealth tax for entrepreneurs. It is important to note that these measures generally require an express request to the tax authorities. Before requesting their application, it is recommended to assess their tax benefit compared to the practitioners’ method, especially when the earnings value is lower than the substance value (for example, when the company is in a loss situation during one or more fiscal years).

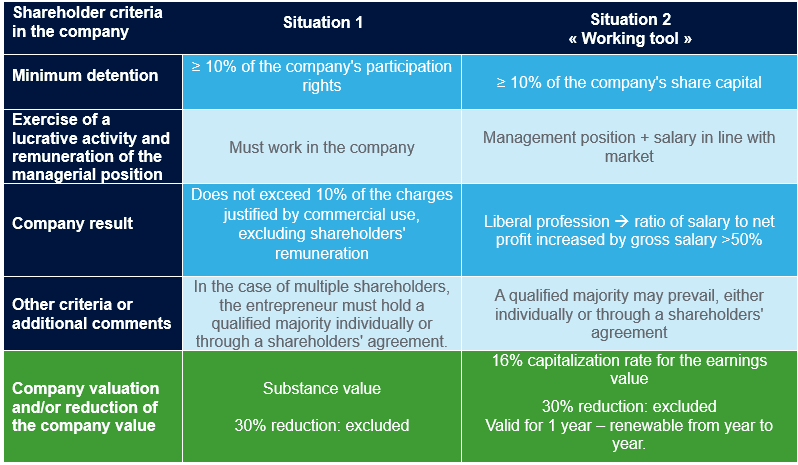

Thus, two specific situations can be summarized. We thought that it appropriate to share an overview of the tax opportunities specific to the canton of Vaud and the related criteria in the table below.

In the situation 1, if the conditions are met, it is possible to request the valuation of the company on the basis of its substantial value (equity).

In the case where the company qualifies as a "working tool" (situation 2) the valuation of the earnings value is significantly reduced by using a capitalization rate of 16% (instead of 8.75% in 2024, for example).

What changes on January 1, 2025

Starting from January 1st, 2025, some significant changes have been made to the tax directive of the Canton of Vaud regarding the valuation of securities classified as "working tools." Here is a summary of the main changes and their implications for entrepreneurs:

- The concept of minimum holding has been changed. Previously, for micro-businesses (5 to 10 employees), a minimum holding of 25% of the participation rights was required. This criterion referred to the size of the company has been removed, offering more flexibility. Additionally, the minimum holding percentage is based on the reference to patrimonial rights rather than social rights.

- In the previous version, the shareholders’ agreement had to specify at least the intention of the holders of rights to manage their shares jointly, including voting rights. This requirement has been abolished, simplifying procedures for shareholders.

- The inclusion of liberal professions. Now, the liberal professions (such as lawyers, doctors, etc.) whose activity depends directly on the holder’s personal work are also included in the criteria. In addition, the threshold for market-compliant remuneration has been lowered: it is now deemed non-compliant if it is below 50%, making the criterion more flexible (previously 70%).

- Restriction on the 30% flat-rate deduction. A new restriction has been introduced regarding the flat-rate deduction. It will no longer be applied if the dividend yield is deemed reasonable.

Conclusion

Do you have questions about the valuation of your unlisted securities or need personalized expertise? Our team of tax experts is available to provide advice tailored to your situation. We help you decipher the tax mechanisms and the specific adjustments in the Canton of Vaud. Contact us for personalized support.

Your direct Contacts!