On March 4, 2024, the Young Socialists of Switzerland (JUSO) submitted a federal popular initiative titled «For a social climate policy – fairly financed through taxes (initiative for a future)», supported by around 110’000 signatures. This initiative proposes a 50% tax on inheritances and gifts exceeding CHF 50 million, starting from the day the initiative is adopted.

Goals and Motivation of the Initiative

Wealthy individuals should bear more responsibility in financing sustainable climate policies. This is the party’s third attempt following the inheritance tax initiative of 2015, which was rejected by 71% of voters, and the 99% initiative of 2021, which failed with 65% of votes. Unlike the 2015 inheritance tax initiative, which included some exceptions for family businesses, the new initiative contains no such provisions. It is estimated that around 2’000 individuals in Switzerland would be affected by this tax.

JUSO expects annual tax revenues of approximately CHF 6 billion. Two-thirds of these revenues would go to the federal government, while one-third would be distributed to the cantons. These funds are intended primarily for the socially equitable fight against the climate crisis and the restructuring of the entire economy. To prevent tax avoidance, the initiative calls for legal provisions, particularly concerning relocation abroad. This is meant to ensure that wealthy individuals cannot escape their tax obligations by moving their residence abroad.

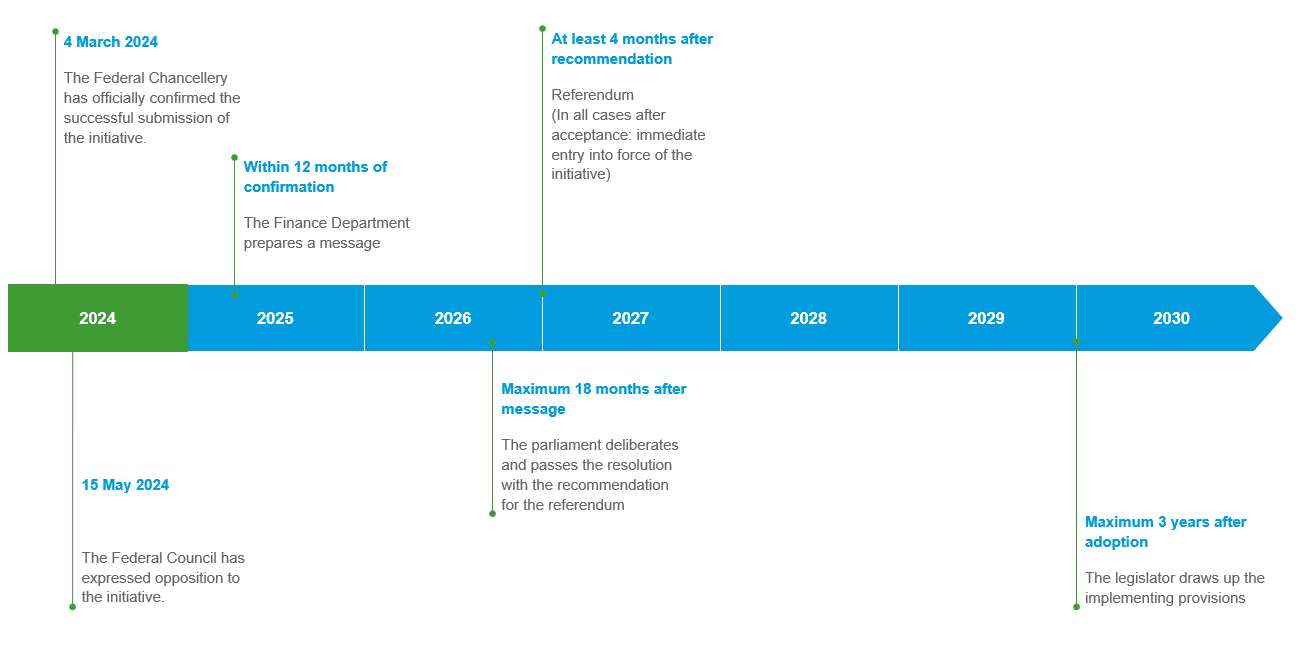

Legislative Initiative Process

The process of a legislative initiative, from its inception to its potential enactment, goes through several stages. The diagram illustrates a typical timeline, summarizing the key steps and deadlines—from the Federal Council's statement, through parliamentary discussions, to a possible referendum at the end of 2026 or the beginning of 2027.

Challenges and Critical Aspects

Cantonal laws regarding inheritance and gift taxes remain in place. Combining existing cantonal inheritance and gift taxes with those resulting from the federal initiative could lead to tax burdens of nearly 100%, depending on the canton. For example, the canton of Basel-Stadt has a cantonal inheritance and gift tax rate of up to 49.5%. Taxation on this scale has confiscatory character and contradicts with various constitutional rights, such as the right to guarantee of ownership and the principle of taxation based on economic capacity. Since the proposed tax exemption of CHF 50 million is estimated to affect only about 2’000 individuals, the inheritance tax initiative has also been criticized for violating the principle of universal taxation.

Another issue is the so-called "dry income" problem. This occurs in cases where no liquid assets are available because the estate is tied up in non-liquid assets such as real estate or businesses. Family businesses could come under significant pressure as there are no provisions for exceptions or deferrals foreseen.

To ensure that taxpayers cannot avoid the new federal tax, the initiative includes measures to combat tax avoidance, including an exit tax upon adoption of the initiative. This could lead to individuals relocating abroad even before the vote. Additionally, the initiative may deter potential residents from moving to Switzerland. The Federal Council estimates that wealth taxes bring in approximately CHF 9 billion for cantons and municipalities, with around 44% of this revenue coming from the wealthiest 1%. Furthermore, around 5% of the wealthiest taxpayers generate two-thirds of the direct federal taxes. Given the risk of relocations abroad and reduced immigration, not only are the additional revenues at risk, but billions in current tax revenues could be lost.

If individuals move abroad, Swiss tax authorities lack the means to enforce tax claims unless there is enforceable wealth remaining in Switzerland. Switzerland does not have a comprehensive network of enforcement assistance abroad, making it difficult to effectively prevent tax avoidance through relocation and the transfer of assets abroad. Although the OECD Model Convention has included a basis for enforcement assistance in Article 27 since 2002, such a provision is currently missing from all of Switzerland's double taxation agreements.

Depending on how the initiative is structured and implemented, conflicts could arise with inheritance tax treaties that Switzerland has with countries such as Finland, the Netherlands, Austria, Germany, Denmark, Sweden, and the United Kingdom. According to these treaties, only the country of residence of the deceased has the right to levy inheritance taxes on movable assets. Specifically, the claim to an exit tax could be limited by these treaties, as international law takes precedence over national law.

A potentially positive aspect, depending on one's perspective, is that the inheritance tax initiative would cover all individuals residing in Switzerland, including those living in cantons without cantonal inheritance and gift tax laws.

Possible Measures

Spouses are treated separately depending to the interpretation of the initiative text, meaning that the CHF 50 million exemption applies per individual. As a result, through an appropriate marital property agreement, the portion of the estate falling into the inheritance upon the death of one spouse could be reduced to fall below the exemption threshold. Ideally, the inheritance at the time of the second spouse's death would again be less than CHF 50 million.

Gifts to children and grandchildren can be structured in a tax-advantageous way through usufruct, depending on how the implementation regulations are designed.

Certain assets located abroad, especially immovable property, are generally exempt from taxation in Switzerland. This is especially the case in countries where Switzerland has signed an inheritance tax treaty. A targeted transfer of assets to countries with inheritance tax agreements can lead to a reduction in the portion of the estate being subject to taxation in Switzerland.

Our Recommendations

The inheritance tax initiative could have profound effects on the tax landscape in Switzerland. We recommend a thorough analysis of the potential consequences of this initiative from both a business and a tax law perspective and suggest planning appropriate measures accordingly. We would be happy to assist you in this matter.

Link to the Initiative Text

You can find the full text of the initiative and further information on the Federal Chancellery’s website (only available in German, French or Italian).

Your Direct Contacts