The Swiss Federal Tax Administration (SFTA) published its updated annual circular letters indicating the safe haven interest rates for loans in CHF and foreign currencies to and from shareholders or related parties applicable for 2025. If the effectively applied interest rates are not within the safe haven interest rates as listed below, then further evidence is required to proof that they are in line with the market interest rates and at arm’s length.

In a decision published in 2024 (see our newsletter here), the Swiss Federal Supreme Court took a position that if a taxpayer applies for intragroup financing interest rate(s) falling below minimum or surpassing the maximum safe haven rates and fails to prove that these interest rates are in line with market prices, the tax authorities shall not be bound to apply the safe haven interest rates but shall be free to determine a market interest rate themselves. While it remains to be seen how this decision will be applied in practice it should be considered when planning intragroup financing.

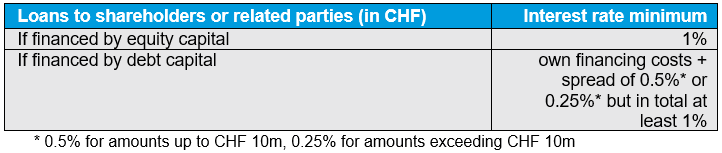

Loans in CHF to shareholders or related parties (asset side)

The minimum interest rates for CHF loans granted by a company based in Switzerland to a shareholder or related party are as follows:

Loans in CHF from shareholders or related parties (liability side)

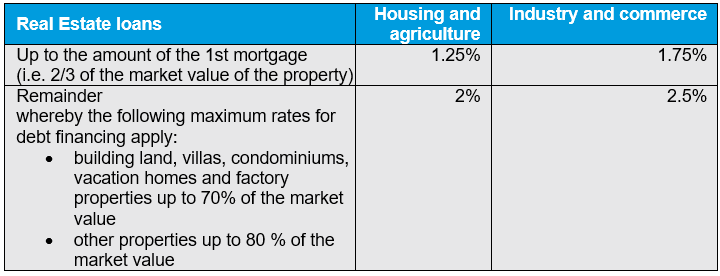

The maximum interest rates for CHF loans received from a shareholder or related party (depending on the use of the funds) are as follows:

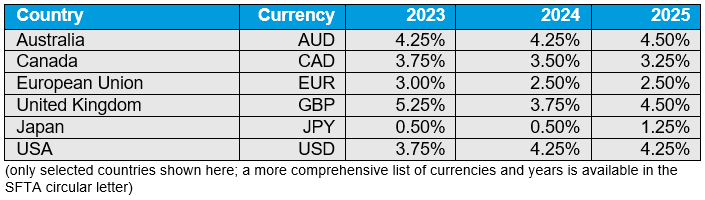

Loans in foreign currencies to shareholders or related parties (asset side)

If loans are not granted in CHF but in a foreign currency, the safe haven interest rates in the table below are to be applied as a minimum interest rate (but at least the interest rate for loans in CHF, should the interest rate for the foreign currency be lower):

The safe haven interest rates are valid provided that the loans are financed by equity. For loans financed by debt capital, a minimum spread of 0.5% has to be added, but in total at least the safe haven rate has to be applied.

Loans in foreign currencies from shareholders or related parties (liability side)

The safe haven interest rates as per the table above are basically also applied as the maximum safe haven rates for loans payable in foreign currencies.

However, for operating loans, the safe haven rates for loan payables can be increased by 2.5% (for amounts up to CHF 1m) respectively by 0.75% (for amounts exceeding CHF 1m) for trading or production companies.

For holding or asset management companies, the safe haven rates for operating loan payables can be increased by 2% (for amounts up to CHF 1m) respectively by 0.5% (for amounts exceeding CHF 1m).

Source: Swiss Federal Tax Administration / Safe haven interest rates

Your Contacts