The valuation of unlisted shares, or the shareholder’s equity stake in companies that are not traded on a stock exchange, reveals special challenges in terms of tax assessment. Unlike listed shares, whose value is easily accessible via the financial markets, the unlisted shares require more complex valuation methods. These valuations have a direct impact on the taxable wealth of entrepreneurs holding shares in these companies, particularly those domiciled in cantons with high wealth taxes.

In this context, many cantons have introduced measures aimed at reducing the tax base of entrepreneurs who hold shares in these companies. This stems from the long-standing discrepancy where the tax valuation of these shares, used to determine taxable wealth, has consistently exceeded their actual market value. How are these valuations made? What flexibility do the tax authorities allow in the valuation of unlisted shares owned by entrepreneurs? Let us examine these questions in more detail below.

Current context

In the current system, the taxable wealth is generally estimated based on the market value of the asset. Market value refers to the price that can be obtained for an asset under normal circumstances. These shares must be valued at the end of the tax year to determine their taxable value. However, the determination of taxable value is difficult when it comes to assets that have no observable market value. In order to harmonize the cantonal tax practices, the Swiss Federal Tax Administration (SFTA) has published the Circular 28, entitled "Instructions on the valuation of unlisted shares for the purpose of wealth tax" (hereinafter: " Circular 28 "). In general, the cantonal tax authorities adhere to Circular 28. However, a deviation from its principles is not excluded, provided that the circumstances relating to the company justify it and that the general principles of taxation are met.

General principle – the practitioners’ method

The Circular 28 prescribes that the commercial enterprises are valued using a standard valuation method, known as the «practitioners' method». This method is based on a weighted average of the following two elements: the earnings value (double weighted) and the substance value (single weighted). To determine the substance value, the company’s equity is considered, including untaxed latent reserves. The earnings value, on the other hand, measures the company's ability to generate profits. It is calculated by averaging the net results of the last financial years, to which a capitalization rate is applied. As an indication, for the 2024 tax year, the SFTA has applied a capitalization rate of 8.75% for the valuation of unlisted shares.

Thus, the practitioners' method can be expressed mathematically as follows:

Exceptions

In accordance with the Circular 28, the exceptions to the practitioners' method are provided in the following cases:

- For real estate companies, holding companies, asset management companies, financing companies and start-ups, the valuation is based solely on their substance value (equity).

- For companies in liquidation, only their liquidation value is considered.

- For companies that are difficult to sell, due to their dependence on a single key individual who holds all or the majority of participation rights, a simple weighting of the earnings value (i.e. not double weighted) and the substance value is applied.

- In case of significant transactions between third parties (sale of more than 10% of shares), the purchase or sale price serves as a reference for the valuation.

Flat-rate deduction (30%)

Specific deductions also apply depending on the shareholding held in the company. Thus, for the minority shareholder representing less than 50% of the shares, a flat-rate deduction of 30% can be applied, provided that no appropriate dividend is distributed. This deduction is granted only if the valuation of the company has been established using the practitioners' method or its substance value.

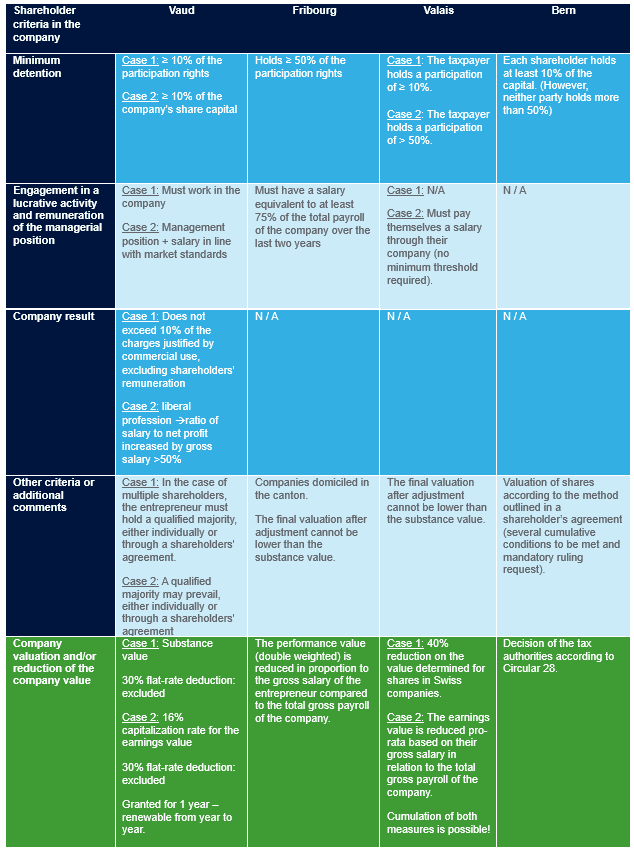

Overview of various tax practices in the French speaking part of Switzerland

Most Swiss cantons have adopted tax measures aimed at reducing the tax burden on Swiss entrepreneurs. Each canton may have its own specificities, which is why we find it useful to provide a brief overview below of the opportunities and the related criteria offered in the French speaking part of Switzerland. Please note that it is generally necessary to submit an express request to the tax authorities to benefit from it. In addition, before requesting its application, it is wise to assess whether this alternative is more favorable in comparison with the practitioners' method (especially when the earnings value is lower than the substance value).

In the Canton of Geneva, the draft law proposing a reduced tax burden on Swiss entrepreneur was rejected in September 2024. As a result, Geneva’s tax valuation are based solely on Circular 28.

In the Canton of Neuchâtel, a cantonal reduction of 60% is applied to the valuation of unlisted shares. However, the tax value before the granting of the reduction is used to calculate the tax rate.

Finally, in the Canton of Jura, the participations in Swiss companies are taxed at a reduced value, corresponding to the gross tax value reduced by 30% of the difference between the tax value and the nominal value.

Conclusion

The valuation methods mentioned above are often subject to debate, and many taxpayers have challenged them up to the Federal Supreme Court. Furthermore, each canton has its own specificities and a margin for negotiation.

Do you have questions about the valuation of your unlisted shares or need personalized expertise? Our team of tax experts is at your disposal to offer you advice tailored to your situation. We help you decode the tax mechanisms and specific adjustments in your canton. Contact us for a customized support.

Your Contacts