")

Update on information to be provided : annual adjustments of pro rata keys “% Global result specific pro rata”

Background

As from 2024, mixed and partial VAT taxable persons need to inform the Belgian VAT authorities upfront of their choice how to organize their VAT deduction. In this respect, they can choose to apply a VAT deduction based upon a general prorate or based upon the so-called “real use method”.

In addition, at the latest on 20 April of the calendar year following the calendar year when transactions have taken place, the VAT authorities must be informed of:

- the definitive pro rata key of the previous calendar year, that will be used as provisional pro-rata key of the ongoing calendar year

- the applied definitive special pro rata keys, and the part of the incurred VAT amounts expressed in %, that

- which has been deducted entirely;

- Which has not been deducted at all,

- and which has been deducted partially.

Further information can be found on the "INTERVAT" VAT return.

Change in 2025: “% Global result specific pro rata”

As from 2025, the “Intervat application in which the above-mentioned information need to be provided, foresees a new box called “% Global result specific pro rata”, in which the global result of the application of the special pro rata keys need to be reported.

Please find below, by means of example, how this box needs to be completed.

A cultural center (non-profit association), generates revenue of which 25% is subject to VAT (cafeteria) and 75% is exempt (organisation of shows). In 2024, the centre incurred various costs on which in total €60,000 VAT was charged:

- €42,000 VAT, for the complete renovation of the cafeteria

(VAT paid under the reverse charge mechanism); - €12,000 VAT, for the purchase of new movable furniture for the concert hall;

- €3,500 VAT relating to the maintenance of a building used for the above-mentioned activities. In this respect a special pro rata key is determined according to surface area used, expressed in m².

Leading to a special VAT pro rata of 15%. - €2,500 of VAT on accounting and miscellaneous invoices. For these costs, a special pro rata calculated as a general pro rata of 25% is applied.

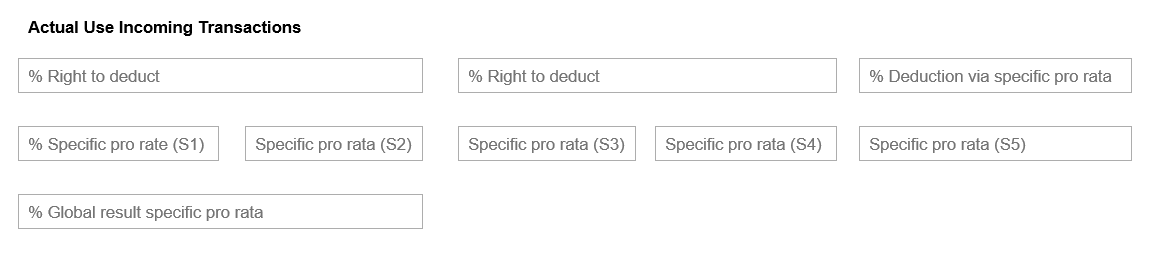

At the latest on 20 April 2025 following percentages need to be reported in Intervat :

- 100% right to deduct: 70% (€42,000/€60,000)

- 0% right to deduct = 20% (€12.000 EUR/ €60,000)

- % deduction via specific pro rata= 10 % ((€3,500 + €2,500 )/ €60,000)

- % specific pro rata: 15 %

- % specific pro rata 25%

- % global result specific pro rata: (€3,500 * 15% + €2,500 * 25%) / (€3,500 + €2,500) =

(€525 + €625) / €6,000 = 19%

If you would require additional assistance in this respect, the RSM Belgium Tax team is at your disposal ([email protected]).

")