Considering the growing concerns over the availability and strategic importance of industrial raw materials, governments worldwide have adopted stricter export control measures. The strategic importance of these materials for green and digital transitions, has led to tighter restrictions, which are driven by geopolitical tensions and national security considerations. This article examines the shift in export restrictions, drawing from the OECD reports on Export Restrictions on Industrial Raw Materials and highlights their impact on businesses that rely on critical materials like lithium, cobalt, and gallium. As countries like China dominate production of such materials, businesses face higher costs and supply disruptions, prompting a push for localized production and strategic autonomy, which is reflected on the introduction of the EU Critical Raw Materials Act.

This article is written by Cem Adiyaman ([email protected]) and Lorena Velo ([email protected]). Cem and Lorena are part of RSM Netherlands Business Consulting Services with a specific focus on International Trade and Strategy matters.

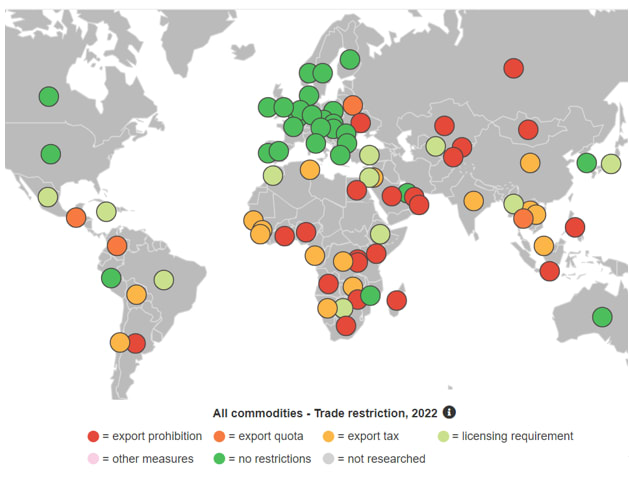

OECD Report on shifting trends of Strategic Raw Materials

The demand for industrial raw materials has increased and is essential for sectors such as renewable energy, electric vehicles, and digital technologies, which is part of the new green and digital transitions. These products are often concentrated in specific countries such as China making global supply chains vulnerable to disruptions. By reviewing the documents submitted by OECD, we see a trend shift in strategic raw materials and the industries they affect. In the past, the key materials studied were lithium, platinum, and rare earths, which have critical use in high-tech industries such as semiconductors, aerospace, and automotive. However, we see that in 2024, the focus has expanded to address the importance of materials for the green and digital transitions. For instance, there is an increased demand for materials such lithium, cobalt and nickel, which are used to produce batteries, gallium that is used in solar panels and titanium that are used in the space and defense sectors.

The OECD has been collecting data on export restrictions on critical raw materials since 2009 and the main trend identified is that export controls on industrial raw materials has increased fivefold between 2009 and 2022. In 2010, export restrictions focused on quantitative export restrictions (quotas), export taxes, and mandatory minimum export prices to preserve national resources and protect local industries, which were mostly seen in China. However, by 2024, the scope of export restrictions has expanded globally, with more countries, including India, Vietnam, Argentina and Saudi Arabia, imposing diverse restrictions such as export prohibitions, licensing requirements and export taxes to protect domestic industries.

Another trend we see is that by 2024, export restrictions as viewed as a tool to manage environmental concerns and promote strategic autonomy in global supply chains for critical industries. Export quotas or bans can be used to stimulate local production of raw materials aiming to lower the domestic prices or reduce global supply with the strategic incentive to attract foreign investment in processing infrastructure.

Business Implications

Considering the high degree of interdependence between the global economy and countries’ reliance on international trade for accessing critical raw materials, the export restrictions imposed can disrupt global supply chains. This is because the availability of critical raw materials is concentrated in a few producing countries such as China and Russia, which are subject to export controls and current geopolitical tensions. For instance, since 2009, there has been a five-fold increase in export restrictions, where 10% of global trade in critical materials is now affected by at least one restrictive measure. As a result, companies across industries, including electronics, automotive, and defense, are experiencing increased production costs and delays, threatening both profitability and innovation timelines. Furthermore, businesses are forced to reassess their sourcing strategies and supply chain management to mitigate the risk of future disruptions.

The dependency on materials like gallium and germanium, which are predominantly produced in China, poses a significant challenge for industries reliant on these inputs. This dependency makes companies vulnerable to price volatility, export quotas, and the potential for sudden supply shortages. In response, businesses are increasingly compelled to seek alternative suppliers, reconfigure supply chains, and even consider nearshoring or investing in local production capacities to safeguard their operations. This shift is especially pressing as geopolitical tensions continue to rise, compounding the uncertainty around the availability of these essential raw materials.

On the other hand, the European Union is aiming to reduce its dependency on Chinese products and technologies by introducing the European Critical Raw Materials Act to support green and digital transitions. This act, in alignment with the OECD’s analysis in its 2024 report, underscores the urgency for businesses to move towards smaller, more controllable, and resilient supply chains, enabling them to better manage both cost and risk. For instance, German car manufacturers are facing mounting challenges competing with Chinese manufacturers due to the scarcity of critical materials needed for production. Additionally, with the implementation of the Critical Raw Materials Act, automotive producers and other industries will need to place greater emphasis on sourcing materials that comply with environmental standards, pushing companies to rethink their product designs, sourcing strategies, and sustainability initiatives to remain competitive and compliant in this evolving landscape.

Forward Thinking

Considering the increasing export restrictions and geopolitical complexities surrounding critical raw materials, businesses must adopt proactive strategies to mitigate supply chain risks. Companies should prioritize diversification of their supply sources, invest in localized production capacities, and explore partnerships in regions less affected by export controls. Additionally, fostering innovation in material substitution, recycling, and circular economy practices can reduce dependence on limited resources. Organizations should also engage with policymakers to stay ahead of regulatory changes, such as the EU Critical Raw Materials Act, ensuring compliance and leveraging incentives that support the green and digital transitions.

Furthermore, nearshoring within Europe will become increasingly important for manufacturers and OEMs. Companies should shift their focus to developing products based on locally sourced raw materials, particularly from resource-rich regions like the Nordics, rather than relying on materials from overseas. This strategic pivot can reduce exposure to supply chain vulnerabilities and geopolitical risks. However, for this approach to succeed, governments must facilitate the process by speeding up the approval of mining permits and providing regulatory support. Simultaneously, companies need to adjust their R&D efforts to align with localized materials and pricing, ensuring their product offerings are sustainable and competitive in the evolving market landscape.

If a company is highly dependent on critical raw materials, it should take immediate action by investigating alternative sources of raw materials in nearby countries and adjusting its supply chain accordingly. This includes focusing on regions with resource availability, such as the Nordics, and incorporating these local materials into product development. By doing so, companies can mitigate the risks of supply disruptions and reduce their reliance on geopolitically sensitive supply chains. Proactive adjustments to sourcing strategies and R&D processes will ensure that products are not only resilient but also aligned with the growing demand for sustainability and localized production.

RSM is a thought leader in the field of International Trade and Strategy Consulting. We offer frequent insights through training and sharing of thought leadership that is based on a detailed knowledge of regulatory obligations and practical applications in working with our customers. If you want to know more, please reach out to one of our consultants.

2: Export Restrictions on Strategic Raw Materials and Their Impact on Trade and Global Supply | The Economic Impact of Export Restrictions on Raw Materials | OECD iLibrary (oecd-ilibrary.org) and OECD Inventory of Export Restrictions on Industrial Raw Materials 2024 | OECD