The recent announcement by President Donald Trump regarding a 25% tariff on goods imported from the European Union (EU) represents a significant pivot in international trade. Trump's historically direct approach to trade wars, previously demonstrated with China, Mexico, and Canada, suggests a volatile period ahead for transatlantic trade relations.

The political climate in Europe is also undergoing a transformation. Germany's newly elected Bundeskanzler, Joachim Merz, along with French President Emmanuel Macron, has publicly expressed a desire to focus more on strengthening the EU's internal market and reducing dependence on the United States. This aligns with the European Commission's Competitiveness Compass, which emphasizes resilience and competitiveness within the single market. Additionally, European Commission President Ursula von der Leyen hinted at warming ties with China during her speech at Davos in January, signaling a potential shift in EU trade strategy towards greater engagement with Asian markets.

This article will provide strategic insights suitable for executive decision-making with a macroeconomic impact horizon of 1–2 years.

This article was written by Mourad Seghir ([email protected]) and Herman Annink ([email protected]). Both Mourad and Herman are consultants with RSM Netherlands Business Consulting with a focus on International Trade & Strategy.

These geopolitical developments create a complex landscape for internationally active businesses, with potential impacts ranging from supply chain disruptions to strategic realignments. Key industries, including manufacturing, logistics, pharmaceuticals, energy, automotive, financial services, defense, and private equity, are poised to experience varied effects depending on how these scenarios unfold.

Macroeconomic Impact

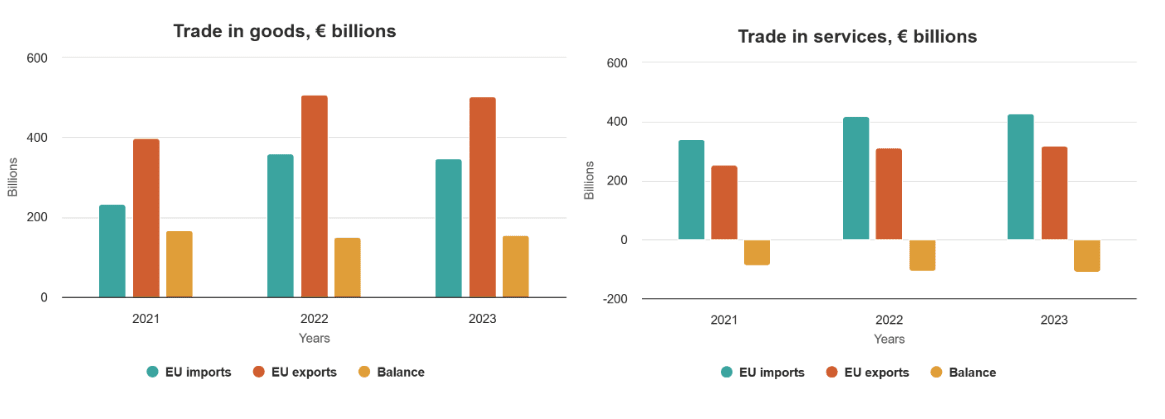

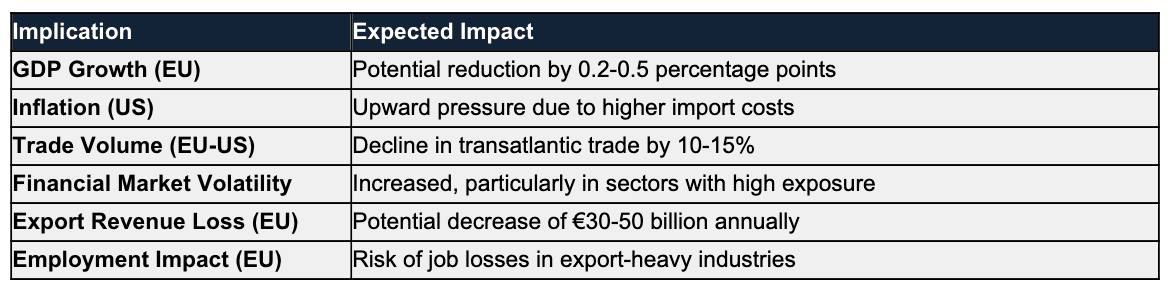

The 25% tariff is expected to disrupt EU–US trade flows, exert downward pressure on GDP growth, and increase inflationary pressures within the U.S. According to the European Central Bank (ECB), the EU is the United States' largest trading partner, with total goods trade amounting to approximately €1.6 trillion in 2023.

Figure: EU trade relations with the United States. Facts, figures (European Commission)

The World Trade Organization (WTO) anticipates a decline in EU exports to the U.S., particularly affecting high-impact sectors such as automotive, machinery, and pharmaceuticals. Key implications include:

The broader macroeconomic implications suggest a shift in trade balances and potential realignment of international supply chains. The ECB's recent analysis warns of potential stagflation scenarios, where economic stagnation is coupled with rising prices, primarily driven by disrupted trade flows and increased costs of imported goods.

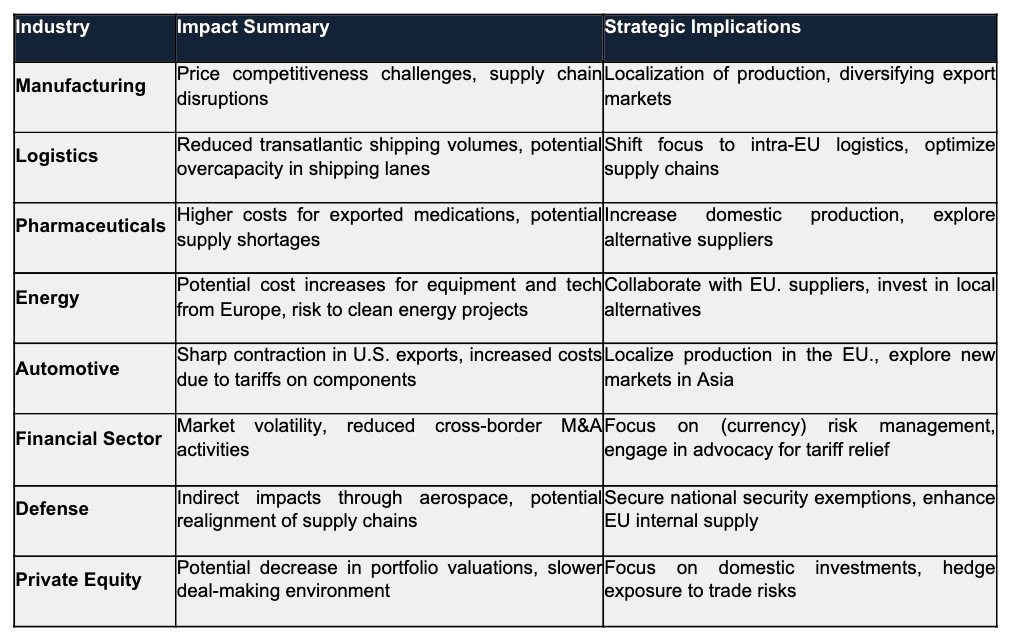

Industry-Specific Impacts

The effects of the 25% tariff will vary widely across industries, depending on their exposure to EU–US trade and their adaptability. Below is a detailed analysis of the potential impact on key sectors:

Sources: European Central Bank (ECB), World Trade Organization (WTO), Eurostat

Strategic Scenarios

1. EU Isolation and Internal Market Focus

In this scenario, the EU prioritizes its internal market to mitigate external economic shocks. By focusing on the Competitiveness Compass strategy outlined by the European Commission, the EU could strengthen internal trade, support regional manufacturing, and reduce dependency on non-EU markets. This approach would involve significant investment in: infrastructure, digital transformation, and sustainability initiatives within the EU.

This strategy also aligns with the European Green Deal, which promotes circular economies and reduced carbon footprints. By isolating its economy, the EU could accelerate green technology adoption and reinforce supply chain resilience. However, this isolation could reduce competitiveness in global markets, especially if protectionist policies lead to higher production costs. Industries such as automotive, pharmaceuticals, and technology could see a pivot towards intra-EU supply chains, reducing exposure to external tariffs but potentially limiting market access and growth opportunities.

2. EU-China Collaboration

Alternatively, the EU could strengthen its economic ties with China, leveraging opportunities in materials, technology, and decarbonization. This strategic shift might be driven by pragmatic considerations, such as China's dominance in critical materials and advanced manufacturing technologies. A collaboration with China could offer EU businesses access to new markets, reduced costs through supply chain efficiencies, and support for the EU’s decarbonization goals through Chinese green technologies.

However, this alignment might exacerbate geopolitical tensions with the U.S., potentially exposing European businesses to secondary sanctions or regulatory challenges. The financial sector could face particular risks if U.S. policies limit transactions with Chinese entities. Nonetheless, industries such as pharmaceuticals, energy, and logistics could benefit from expanded trade opportunities and collaborative innovation projects, particularly in green technology and digitalization.

Forecasting

Our latest data-driven analysis highlights significant economic risks from declining EU exports to the U.S., rising inflation in the U.S., increased unemployment in the EU, and heightened financial market volatility.

- Export Decline: EU exports to the U.S. could drop by 10-15%, translating into a potential €50 billion annual loss for EU companies, primarily impacting automotive, machinery, and pharmaceuticals sectors (Source: WTO).

- Inflation Impact: The U.S. could see inflation rise by up to 0.5%, as import costs increase which has macroeconomic implications on future borrowing costs and CPI/PPI. (Source: U.S. Federal Reserve).

- Job Market Pressure: The EU labor market may experience a 0.3% rise in unemployment, with significant job losses in manufacturing and export-oriented services (Source: European Labour Authority).

- Financial Market Volatility: Market indices in both regions could see increased volatility, particularly in equities related to exposed sectors (Source: IMF). Additionally, this will increase intra EU capital investments from non-US firms.

Forward thinking

Based on our forecasting we see the need for strategic measures such as risk mitigation, market expansion, supply chain adaptation and investments in innovation.

The introduction of U.S. tariffs on EU imports presents a nuanced challenge for internationally active businesses. Despite short-term disruptions, companies that adapt through risk management, market diversification, and supply chain innovation can build resilience. Staying agile, leveraging insights, and aligning with EU sustainability and tech goals will help businesses navigate risks and seize growth opportunities.

RSM is a thought leader in the field of Strategy and International Trade consulting. We offer frequent insights through training and sharing of thought leadership based on a detailed knowledge of industry developments and practical applications in working with our customers. If you want to know more, please contact one of our consultants.