On February 2, 2017, the Economic Affairs and Taxation Committee of the Council of States submitted the parliamentary initiative "System Change in Homeownership Taxation"In the 2024 winter session, Parliament ultimately decided to abolish the imputed rental value.

Current System

Owners of self-occupied properties must declare an imputed rental value in their annual tax return. The imputed rental value was introduced in accordance with the constitutional principle of equal treatment and serves to balance the fact that tenants cannot deduct rent payments, which are considered living expenses, from their taxable income. It is important to note that the imputed rental value is not fictitious income but rather income without an actual cash inflow ("dry income").

All income related expenses can be deducted from the imputed rental value. These include maintenance costs for preserving the property's value, administrative expenses, investments that promote energy efficiency, environmental protection and heritage conservation, as well as mortgage interest payments.

Future System

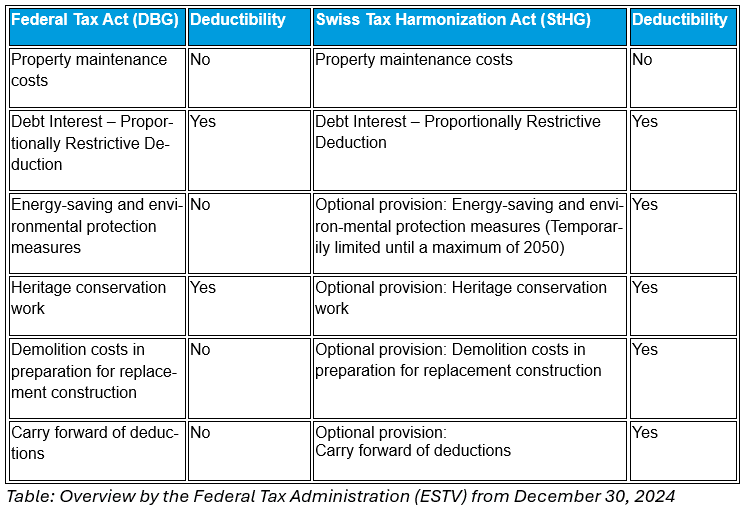

In the future, imputed rental value will no longer exist, neither for primary residences nor for secondary properties (e.g., vacation homes). This change will impact the deductible expenses allowed under the current system, with a distinction between the federal and cantonal/municipal levels. The planned deductions are as follows:

As part of the homeownership promotion, individuals purchasing self-occupied property for the first time can claim a so-called first-time buyer deduction. The deduction amounts to CHF 5,000 in the first year for single individuals and CHF 10,000 for married couples, decreasing linearly over the following nine years. In the 11th year, no deduction is available anymore.

In the event of a system change, the mountain and tourism cantons would also have the option to introduce a property tax on secondary residences at the cantonal level to provide financial relief.

Pros and Cons

The following arguments are regularly cited for a system change:

- No preference for homeowners: While the imputed rental values are regularly set up to 40% below the market rental value, the income-related expenses can be fully deducted at market value. The Federal Court justifies the current law's usual preference for homeowners with the (weak) argument of constitutional promotion of homeownership.

- Decreasing private debt: If mortgage interest is no longer deductible, individuals will acquire homeownership with less debt and more equity. This follows recommendations from the OECD and the IMF, which view the high private debt of the Swiss population as a risk to financial stability.

- International acceptance: Only a few European countries have an imputed rental value taxation. By changing the current system, Switzerland would align itself with the majority of European countries.

- Elimination of the pensioner issue: For retirees with low income who have largely repaid their mortgage, the current system leads to an disproportionately high tax burden. A system change would address this issue.

The following arguments are made against a system change:

- Pro-rich: Individuals who can finance their owner-occupied property with a high proportion of equity have an advantage over homeowners who need to take on more debt, as the latter cannot fully deduct or no longer deduct interest on the debt.

- Shadow economy: Experts fear that a system change will increase undeclared work. Previously, homeowners had a system-based interest in receiving correct and complete invoices, as without documented proof, no deductions could be made in the tax return. In the future, this incentive would disappear, and a correct invoice would "only" result in tax and social security contributions for the tradespeople. The tax losses resulting from this are estimated to amount to CHF 1.7 billion.

- Declining construction industry: In the case of a system change, property maintenance costs would be brought forward, leading to a sharp decline in orders after the introduction. In the medium to long term, a downturn in the construction industry is also expected, partly due to increasing undeclared work, and homeowners may delay or even avoid repairs, renewals, renovations, etc. (risk of neglect).

What’s next?

Due to the planned introduction of a property tax on secondary residences, a referendum is required. Such a vote is expected to take place no earlier than autumn 2025. The transition period for the implementation is still pending but will be at least 2 years.

Our Conclusion

The imputed rental value has long been criticized and is met with little acceptance, particularly among homeowners, within the Swiss population. As such, the current system is unlikely to be sustainable in the future. It would be desirable if the proposed system change creates a more balanced relationship between tenants and homeowners.

Should you have any questions regarding the system change or the deductibility of your property maintenance costs, either before or after the system change, our experts are happy to assist you.

Your direct Contacts